Given that January’s figures put us back on INFLATION WATCH in America, this week’s releases of February’s Consumer Price Index and Producer Price Index were eyed to see if those higher numbers from January would continue, which could drive the Federal Reserve to keep raising interest rates throughout the first half of 2023.

First up was the CPI, and it leveled off from the January increase that alarmed many on Wall Street.

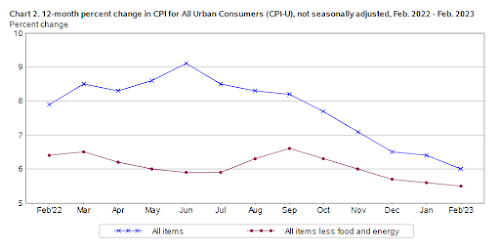

The Consumer Price Index (CPI) revealed headline inflation rose 0.4% over last month and 6% over the prior year in February, a slowdown from January's 0.5% month-over-month increase and 6.4% annual gain. Both measures were in-line with economist expectations, according to data from Bloomberg.

The 6% jump in inflation marks the slowest annual increase in consumer prices since September 2021.

"Core" inflation, which strips out the more volatile costs of food and energy, rose 0.5% over the prior month in February and 5.5% over last year, marking the smallest 12-month increase since December 2021. Economists had estimated "core" inflation would rise 0.4% on a month-over-month basis and increase 5.5% compared to February 2022.

You can see the steady decline in the 12-month price change since inflation peaked in June.

And then going inside that 0.4% increase in CPI, I see positive trends. February’s 0.3% increase in “food at home” was the smallest since May 2021, with fresh fruits and vegetables going down, and egg prices starting to come back toward earth with a February fall of 6.7%.

The “core” increase of 0.5% also is misleading, as much of that is due to the shelter category, and

Investopedia is among those who remind us that higher “shelter” costs (reflected in a measure called Owners’ Equivalent Rent, or OER) aren’t necessarily higher costs for people in the real world.

For most goods and services, the process of recording prices is relatively simple: The bureau sends someone to a store, or calls a business, to see what they are charging for a bag of rice or to send a plumber out to repair a leaky faucet. Recording housing prices isn't as straightforward. The bureau measures actual rental rates for houses, and, using that data, estimates how much owner-occupied houses would rent for if they were put on the market.

“It's a little bit of a fuzzy metric,” said Ryan Sweet, chief U.S. economist at Oxford Economics.

OER is effectively the rent that the homeowner is giving up by living in their house instead of renting it out. It’s influenced by housing prices, but not directly tied to it….

As a result of its methodology, the all-important OER measure tends to lag behind movements in nationwide home prices by about a year. It took a long time for the pandemic-era surge in home prices to show up in the Consumer Price Index, and it will likely take a long time for the recent cooling of the housing market to show up as well.

So this will also mean that CPI will cool down in the coming months based on this lagging OER measure alone. And given that many Americans are locked into fixed-rate mortgages and/or year-long leases, it is unlikely that they actually paid 0.8% more in shelter costs in February 2023.

Then on Tuesday,

we got information on Producer Prices, and that had even better news for those worried about inflationary pressures.

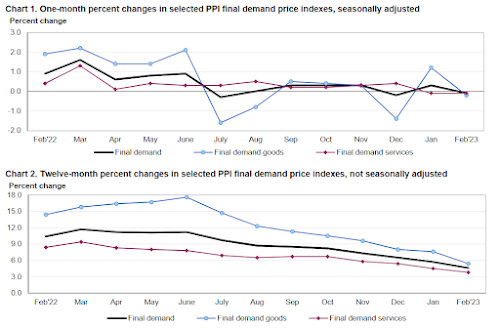

A key measure of inflation fell dramatically in February, according to the latest Producer Price Index, which tracks what America’s producers get paid for their goods and services.

Producer price increases slowed to an annual pace of 4.6% last month, significantly lower than the downwardly revised 5.7% in January, the Labor Department reported Wednesday. February prices fell by 0.1% after rising by a downwardly revised 0.3% in January.

Economists surveyed by Refinitiv had been expecting the 12-month rise in wholesale prices to slow to a 5.4% increase.

Taking out the often volatile food and energy components, core PPI also notched some stark declines: Annual price increases dropped to 4.4%, and the index was unchanged from the month before (0% growth). Those are down from January’s downwardly revised 5% annual price gain and 0.1% monthly increase.

So businesses aren’t seeing their costs for products in going up. That declining trend in PPI has been going on since June, with no one month having an increase in final demand above 0.3%.

The total increase in PPI in the last 8 months is less than 1% for the last 8 months measured, which translates to around 1.5% on an annual basis – below the Fed’s already-low 2% goal.

Of course, these CPI and PPI reports predate last weekend’s closures of a couple of banks , whose problems seem related to the Fed’s higher interest rates leading to those banks’ bond holdings being worth less, and lower amounts of lending (because it’s more expensive to borrow money).

And the banking fears now feed back into INFLATION WATCH,

as oil plummeted Wednesday. Futures dropped down below $67 a barrel on Wednesday before recovering some losses and closing over $68. That's a lower closing price than we had at any time in 2022.

The news of the last week shows the folly of the Fed chasing last year’s inflation by continuing to increase rates today. Not only do we have 8 months of calmer inflation with little to spark it back up, but we also have banks and other businesses suffering because interest rates have gone up so fast and so quickly.

Well past time for Jerome Powell to stop the 1970s mentality, deal with 2023’s reality, and BACK OFF.

No comments:

Post a Comment