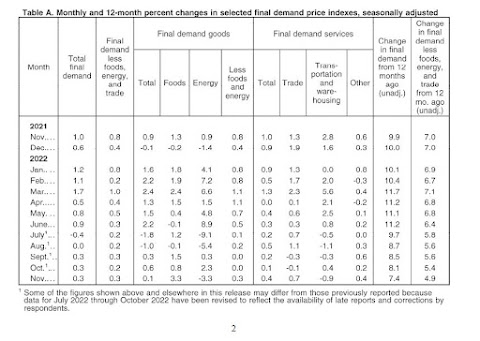

Wholesale prices rose more than expected in November as food prices surged, dampening hopes that inflation could be headed lower, the Labor Department reported Friday. The producer price index, a measure of what companies get for their products in the pipeline, increased 0.3% for the month and 7.4% from a year ago, which was the slowest 12-month pace since May 2021. Economists surveyed by Dow Jones had been looking for a 0.2% gain. Excluding food and energy, core PPI was up 0.4%, also against a 0.2% estimate. Core PPI was up 6.2% from a year ago, compared with 6.6% in October.Not great on the topline. But when I looked at the full report, I didn't see much to be concerned about. The media report of "food prices surging" in November (by 3.3% overall) was largely contained to three types of food. Change in producer prices, November 2022

Fresh/dry vegetables +38.1%

Fresh eggs +26.0%

Beef + veal +3.6% That helps explain why you might be seeing absurd egg and produce prices at the grocery store, especially since both of those types of products have had double-digit increases in producer prices in each of the last 3 months. But beef/veal producer prices are still down 3% compared to July, and other food products declined in November, including like chickens (down for 5 straight months), dairy products (down 4 of the last 5 months), and grains (down each of the last 2 months). In addition, producer-level inflation has been tame since the middle of the year, with a TOTAL change of 0.5% since June, with no month with a core price increase above 0.3% since May, and year-over-year inflation at its lowest point in the last 12 months.

No comments:

Post a Comment