As part of

the monthly income and spending report for October, there was this interesting bit of news.

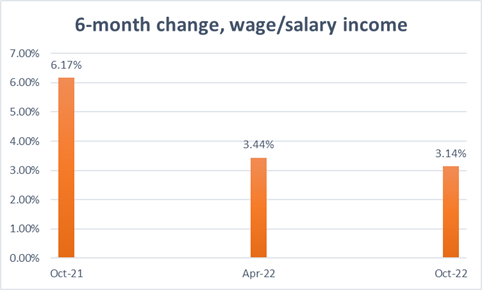

In addition to presenting updated estimates for the third quarter, today's release presents revised estimates of second-quarter wages and salaries, personal taxes, and contributions for government social insurance, based on updated data from the Bureau of Labor Statistics Quarterly Census of Employment and Wages program. Wages and salaries are now estimated to have increased $132.5 billion in the second quarter, a downward revision of $50.4 billion. Personal current taxes are now estimated to have increased $43.0 billion, a downward revision of $9.4 billion. Contributions for government social insurance are now estimated to have increased $19.7 billion, a downward revision of $6.5 billion. With the incorporation of these new data, real gross domestic income is now estimated to have decreased 0.8 percent in the second quarter, a downward revision of 0.9 percentage point from the previously published estimate.

Other than the real GDI numbers, none of those numbers are adjusted for inflation, which indicates that salaries and wages went up by a notably smaller amount than we knew. And it resulted in a notable downshifting of income growth in wages and salaries as inflation picked up in the Winter of 2021 and Spring of 2022.

Some of that reflects job growth also downshifting as unemployment went under 5% and then 4%. But it also indicates that wages weren't as much of a price/demand pressure as we knew in the 2nd and 3rd Quarters of 2022, which helps to explain the big growth in profits.

I got your 2022 inflation RIGHT THERE!

And now that inflation is subsiding

after the election in the latter part of 2022, the declines that workers may have dealt with earlier in the year are turning back into gains, and real consumer spending is benefitting.

....Disposable personal income (DPI) increased $132.9 billion (0.7 percent) and personal consumption expenditures (PCE) increased $147.9 billion (0.8 percent).

The PCE price index increased 0.3 percent. Excluding food and energy, the PCE price index increased 0.2 percent. Real DPI increased 0.4 percent in October and Real PCE increased 0.5 percent; goods [consumption] increased 1.1 percent and services increased 0.2 percent.

These would be good numbers to continue for the end of 2022 and early 2023, and would resemble

the "soft landing" that Fed Chair Powell and others say they want.

What also would help would be in not having nominal and real interest rates be so high that it accelerates defaults and causes a cascade of financial difficulties. Especially given that the same report showed that the US savings rate had dropped even lower due to the lower revisions on wage/salary income, we don't need to be adding onto the stress with more layoffs and excessively high interest payments.

So Jerry and the rest of the Fed should lay off on further rate hikes for 2023 if they're serious about a steady, stable economy. Once again, 4% inflation and wage growth >>>> 5% unemployment to me, and we need policymakers to have that bias as well.

No comments:

Post a Comment