Personal income increased $50.2 billion (0.3 percent) in September according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) increased $55.7 billion (0.3 percent) and personal consumption expenditures (PCE) increased $24.3 billion (0.2 percent).

Real DPI increased 0.3 percent in September and Real PCE increased 0.2 percent. The PCE price index decreased less than 0.1 percent. Excluding food and energy, the PCE price index increased less than 0.1 percent….

Personal outlays increased $23.0 billion in September (table 3). Personal saving was $1.38 trillion in September and the personal saving rate, personal saving as a percentage of disposable personal income, was 8.3 percent (table 1).

That’s a whole lot of “meh” on the income side, but a weak reading on spending. It’s the smallest increase in 7 months (+0.15%), and follows a similarly soft $30.8 billion increase in August. With the consumer being one of the few things keeping the expansion afloat as it hits year 11, that is not a good sign going forward.

Even worse was that the income growth was skewed higher by a one-time assist in the form of federal subsidies.

Farm proprietors’ income increased $23.3 billion in August and $12.1 billion in September; payments associated with the Department of Agriculture’s Market Facilitation Program were substantial contributors to both increases.

Add in the declining price of goods and wages and salaries only accounting for $3 billion of that $50 billion increase in incomes, and that doesn't seem like an economy where there are a lot of sources of organic growth.

The Chicago Purchasing Management Index sank to 43.2 in October from 47.1 in the prior month. This is the lowest level since December 2015. Economists has expected a reading of 48.3, according to Econoday.

Any reading below 50 indicates deteriorating conditions.

What happened: New orders declined to 37, the lowest level since March 2009. Order backlogs saw the largest monthly decline.

New orders sliding hard and fewer backlogs to make up the difference are awful harbingers for the future. It's especially bad news for manufacturing-heavy Wisconsin, which already was in bad shape, according to the Federal Reserve Bank of Philadelphia.

With GDP growth in Q3 slipping below 2% and several other reports this week indicating an economy that might be slowing even more than that, it sure makes tomorrow's jobs report for October into a big deal. In 2019, job growth has slowed, but we haven't seen jobs being lost or unemployment go up. If that starts to happen, or even if job growth falls below 100,000, the spiral may become very hard to stop.

The Commerce Department on Wednesday said the economic activity in the U.S. grew at an annualized rate of 1.9% in the third quarter, down slightly from the 2% print in the second quarter. Economists polled by Dow Jones had expected the economy to grow at a 1.6% rate.

The better-than-expected print was the result of continued consumer spending as well as government expenditures, the government report said. Personal consumption expenditures, a gauge of spending by American households, rose at a 2.9% annualized rate while government spending grew at a 2% rate.

Growth in gross private domestic investment continued to decline in the three months ended September 30 with a read of -1.5%, but far better than the -6.3% contraction in the second quarter.

So continued declines in investment (business) spending and consumer spending slowing from 4.6% growth to 2.9% while government spending keeps growing is the mark of an economy in decent shape? Not so sure about that.

Especially when I look at one particular area of the economy dealing with goods. Because part of the consumption “growth” in real GDP in the industrial sector for Q3 is actually a sign of weakness – price deflation. And it’s worse on the business and trade sides.

This means that real (inflation-adjusted) GDP is higher than the actual growth in spending and trade for these industrial sectors.

So if these industrial businesses are getting lower prices and fewer sales, how are they going to avoid layoffs and/or stay in business? Especially when prices keep rising for consumer services (+2.6%) and residential construction (+3.3%)?

The other thing I want to point out about today’s GDP report is that it reiterates how 2019’s growth is sputtering back to the levels of 2015-2016 that Donald Trump claimed he was going to improve from. Let’s look at GDP growth that takes out the change in government spending (which has grown in the time of Trump), and the effect of inventories.

If you look at the chart of those figures, you’ll see that underlying growth isn’t any different now than when some blue-collars thought electing Trump would “Make America Great Again” by improving the economy. In fact, private sector GDP growth has been under 1.6% for 3 of the last 4 quarters.

You can also see that there is no real difference in growth for the last half of 2017 and the first half of 2018, despite the GOP Tax Scam being passed into law at the end of Q4 2017. And now growth has fallen back to trend after that one-time bump.

Even if you include added government spending and the inventory effect, the last 12 months have only netted 2.0% growth. That’s no different than what we had 3-4 years ago, when Trump took advantage of economic softening to convince some people that he could make things better than what they were experiencing in November 2016.

So what’s going to keep things going with fiscal stimulus ending in the US as deficits rise to $1 trillion, and job growth slowing down? The Fed can try to pump up the stock market and encourage more borrowing by printing money and lowering interest rates (including another 0.25% cut today), but is that going to translate over into the real economy? Doubtful, and there would be more risk of becoming a major recession if things go south.

I’m not buying the happy talk from the financial media, and the numbers in today’s GDP report should be seen as more evidence of a full-employment economy slowing as the US expansion starts its 11th year. The real question is whether that slowing becomes a full-fledged stall and decline for 2020, and my guess is that future jobs reports (including Friday’s release for October) will be a better answer of that question than what we will see from Wall Street.

EDIT- And here's Paul Krugman to remind us that US GDP may tell a much different story than you see in your part of the country.

The meh GDP numbers won't help Trump next year. But what should really scare him is his utter failure to boost manufacturing in swing states pic.twitter.com/x4RkrSnSjS

Tomorrow, the Wisconsin Joint Finance Committee will discuss several items that go over how to use certain sources of money to deal with new initiatives and reallocations of a few funds. Two of these items involve certain infrastructure improvements that should remind us how a couple of foolish stunts in the opening months of the Walker Administration continue to hurt us to this day.

The first item has to do with the state’s initiative to expand broadband access, particularly in rural areas. The Public Service Commission oversees the grant, and they are looking for more support in doing those duties. As the Legislative Fiscal Bureau notes, Governor Evers’ first budget included a big boost in funding for the program, even if it wasn’t everything Tony wanted.

In [the 2019-21 State Budget], the Governor had recommended $74.6 million in increased grant funding, which would have included: (a) $50.4 million in general purpose revenues (GPR) in a new biennial appropriation, with $20 million GPR as annual base funding; (b) $24.2 million in federal e-rate funds transferred on a one-time basis from DOA in the biennium. Changes by the Committee deleted proposed GPR funding and instead transferred $22 million to the USF from federal e-rate funds each year, but only on a one-time basis in the 2019-21 biennium. These funds are in addition to unencumbered amounts from other USF SEG appropriations, which are transferred to broadband expansion grants for use the following year. PSC is provided at least $2 million each year from the USF, should transfers not reach that amount, for which PSC can make assessments to ensure a minimum grant funding level each year.

Even though the GOP-led Joint Finance Committee turned down Evers’ big ask of $50 mil, the $25 million we will grab from the Universal Service Fund to expand broadband next year is more than the total of $20.2 million for broadband that was set aside during Scott Walker’s entire tenure in office. And most of that $20 million under Walker was only set aside in Scotty’s last 2 years, as he desperately tried to make people forget how far behind we were.

The LFB says that over the 6 years the broadband expansion program has been around, it has received grant applications asking for more than 3 times the money that was made available between 2013 and 2019. Because the number of applications and funds for broadband expansion grants have gone up and will go up further under the newly-expanded program, the Evers Administration and the PSC are asking for another person to handle these duties. The idea is that if this new staffer allows grant applications to be processed faster, the sooner broadband will be up and running in more parts of the state.

PSC staff argue an additional 1.0 position remains necessary to adequately complete all tasks associated with grant management, including: (a) monitoring activities under open grants; and (b) drafting grant amendments to address changes in projects. PSC staff contend additional grant oversight is needed to maintain sufficient fiscal controls of grant expenditures. PSC staff also note the number of grants awarded each cycle has generally increased, particularly as additional funds have been appropriated to the program. Although grant awards have not yet been made for the 2019- 21 biennium, Commission staff expect that the total amount of awards will be larger, and the complexity of projects will be higher, as remaining unserved or underserved areas likely require relatively larger allocations of funding to establish broadband infrastructure.

PSC staff report grants typically have a two-year execution period, with extensions possible for good cause. Reimbursement and closing may take additional time. As such, grants awarded throughout the 2019-21 biennium will likely be open into the 2021-23 biennium, and perhaps as late as the beginning of the 2023-25 biennium.

Let’s see if the GOPs on Joint Finance try to hold this up, or monkey with the money in some other fashion that tries to hamstring the build-out of infrastructure that is necessary for communities to compete as we go into 2020.

There’s also another item that deals with an upgrade that could have been done by the Walker Administration several years ago – the purchase of more Amtrak train cars between Milwaukee and Chicago. This would be done by using money that has been already set aside to improve rail infrastructure and vehicles.

As shown in the table below, of the $89,000,000 in total bonding appropriated for passenger rail development projects, $78,904,300 has been approved for use in prior action by the Committee, including: (a) $10,000,000 for renovation of the Milwaukee Intermodal Station and (b) $68,904,300 for costs related to the purchase and delivery of two passenger rail car sets from Talgo and subsequent settlement. Of the bonding amounts approved by the Committee, the Department has expended only $67,430,200, including: (a) $8,021,300 on the renovation of the Milwaukee Amtrak station, including train shed improvements, and (b) $59,408,900 on costs associated with the Talgo contract and settlement. Accordingly, $21,569,800 in existing passenger rail bonding remains unissued. Use of the $21,569,800 in unissued bonding authority requires the approval of the Joint Finance Committee. In addition, $25,000,000 SEG amount appropriated under Act 9 (not shown in the table) is available for the purposes of the passenger rail development program and does not require approval from the Joint Committee on Finance.

The rail cars are needed, as the Hiawatha line between Milwaukee and Chicago continues to grow, resulted in crowded conditions in aging rail cars. Buying the new train sets would add seating capacity, and WisDOT also says the new train sets could save money in the long run through efficiency and less need for maintenance and other repairs.

Ridership on the Hiawatha line grew from 809,785 during the 2015 fiscal year to 880,227 in 2019, representing a 8.7% ridership increase over that period and a 2.1% annual average rate of growth. According to DOT, ridership growth during this period contributed to an increase in the number of trains experiencing near-capacity or over-capacity conditions during peak travel hours. The Hiawatha line currently experiences standing room only conditions on an average of 19 trains per month, mostly on weekdays. In peak summer months, some trains operate with more than 50 standees, which can pose safety concerns. The overcrowding experienced on the Hiawatha will require DOT and Amtrak to add a 7th coach car to all train consists by 2021-22 to accommodate these passengers which would generate additional costs in excess of the current Amtrak contract. The procurement of the new equipment associated with this request would eliminate the need for the addition of the 7th coach cars and NPCUs because the new cars would cumulatively provide 60-67 additional passenger seats.

The Department indicates in its request that the current equipment in use for the Hiawatha service is costly to operate and maintain because of its age. The Horizon coaches, Amfleet coaches and NPCUs are expected to require maintenance overhauls in the next five years in order to maintain a state of good repair. Given the equipment age and multiple overhaul cycles already performed for both the NPCUs and the coach cars, DOT states that these components are at, or past, a point where the life cycle cost of maintaining the assets is higher than the cost of replacing them, thereby placing them outside the definition of “state of good repair” as established in Federal code. In addition, because the old Horizon coaches and NPCUs would be replaced with new single-level coach and cab-coach cars, operating and maintenance cost savings for the Hiawatha service would be substantial. Analyzed over a 20-year study period, Quandel Consultants, LLC performed a benefit-cost analysis to support DOT's federal grant application for the Next Gen equipment acquisition project. The Quandel study estimates that the operating and maintenance cost savings of procuring the Next Gen equipment equates to $27.70 million in benefits, discounted at a seven percent rate. This benefit figure does not include fuel savings or emissions reductions that would result from having Next Gen cab-coach cars that weigh 91 tons less than the current NPCUs and Next Gen coach cars that weigh 25 tons less than the Amtrak Horizon coaches.

Seems like a no-brainer to take the new train sets, but how to pay for it? As you see above, the current state budget added another $25 million in cash for passenger rail, but the LFB notes that the money has been targeted for another Milwaukee project that would make it easier to have more trips on the Hiawatha each day.

Under [the 2019-21 State Budget], DOT was provided $25,000,000 in SEG funding for passenger rail development that does not require JFC approval. On October 14, 2019, the Department applied for a $26.0 million federal grant from the FRA to construct a bypass in Milwaukee's Muskego Yard that would route freight trains away from the downtown Milwaukee train station and involve signal, bridge and track upgrades. The Muskego Yard project is one component of a larger, multi-year project to increase the frequency of Hiawatha service between Milwaukee and Chicago. If awarded, the grant would require a $20.0 million state funding match and $8.0 million in funding from Amtrak. Because the Muskego railyard is largely privately owned by Canadian Pacific, most of the project costs would likely not be bond eligible. As a result, DOT would likely need to provide the federal funding match from the $25.0 million SEG appropriation.

So the question is whether to use some of the $25 mil in cash on the new railroad cars, and not borrow for it, or to borrow the money for the rail cars, and set aside the cash in case the grant for the freight train bypass goes through. It also could lead to some interesting insight.

Of course, both of these topics would have been taken care of long ago IF SCOTT WALKER WOULD HAVE JUST TAKEN THE STIMULUS MONEY FROM THE OBAMA ADMINISTRATION 8 ½ YEARS AGO. But noooo, Koch's boy had to try to spite the Black Man in the White House because…it would have made the economy too good for Obama re-election chances in 2012?

Never forget how the inactions of Governor Dropout and the rest of the ALEC Crew continue left us behind on joining the 2010s for infrastructure, and how much more we have to spend now to try to catch up. Tomorrow’s Joint Finance Committee meeting should remind us all as to how clueless and short-sighted today’s GOP is, and why they can’t be allowed to govern anything significant for a long while.

I had wondered when we’d see the year-end budget figures from the Trump Administration, because the Fiscal Year ended nearly 4 weeks ago, and last year’s final total came out on October 15.

The U.S. Treasury on Friday said that the federal deficit for fiscal 2019 was $984 billion, a 26% increase from 2018 but still short of the $1 trillion mark previously forecast by the administration.

The gap between revenues and spending was the widest it’s been in seven years as expenditures on defense, Medicare and interest payments on the national debt ballooned the shortfall…

Annual deficits have nearly doubled under President Donald Trump’s tenure notwithstanding an unemployment rate at multidecade lows and better earnings figures. Deficits usually shrink during times of economic growth as higher incomes and Wall Street profits buoy Treasury coffers, while automatic spending on items like food stamps decline.

Two big bipartisan spending bills, combined with the administration’s landmark tax cuts, however, have defied the typical trends and instead aggravated deficits. The Congressional Budget Office projects the trillion-dollar deficit could come as soon as fiscal 2020.

Most of the numbers match up with what we saw from the CBO’s estimate from 3 weeks ago, so there isn’t much to discuss further on that subject. But I do want to reiterate how far away we are from what was projected before the GOP Tax Scam was passed into law at the end of 2017.

For 2019, tax receipts were up a bit vs 2018. But it wasn’t the GOP Tax Scam “paying for itself”, but instead mostly due to payroll taxes for Social Security and Medicare. Oh, and also because of an increase in corporate revenues that doesn’t come close to the 40% drop we had in 2018 due to the Tax Scam, and an increase in tariff revenue that still barely covered the $28 billion we are giving to farmers affected by tariffs.

Change in revenue , FY 2019

Payroll Taxes +$72.4 billion

Individual Income Taxes +$34.3 billion

Customs Duties/Tariffs +$29.5 billion

Corporate Income Taxes +$25.5 billion

Excise Taxes +$5.0 billion

Estate Taxes -$6.3 billion

Miscellaneous -$25.9 billion TOTAL CHANGE +$133.4 BILLION (+4.0%)

This is a good explanation of the decline in projected revenues that has resulted from the Tax Scam.

Here is how actual FY19 revenue came in compared to the pre-Trump tax cut projections (CBO, June 2017):

If you compare to the Trump Administration's estimates from July, we actually came up short on estimated revenues by $10.2 billion, and the reason why is hilarious - because the Trump Administration overestimated tariff revenues by nearly $11 billion! While spending was significantly up in 2019 (a boost to GDP that Republicans don’t want to talk about), we still spent $26.4 billion less than anticipated, so we snuck under the $1 trillion estimate by $16.25 billion.

Total receipts in 2018 were $8 billion (or 0.2 percent) lower than what CBO initially projected, and receipts in 2019 were $28 billion (or 0.8 percent) lower. In percentage terms, the differences between actual and projected receipts were larger for individual and corporate income tax receipts than for total receipts (see Table 1). Since April 2018, CBO has published four subsequent revisions to its revenue projections; together, those revisions reduced projected revenues over the 2018–2028 period by $700 billion (or 1.5 percent).

Revisions of that size are not unusual. Revenue projections are inherently uncertain, and actual outcomes would differ from CBO’s projections even if no changes were made to current law. In analyzing its baseline projections of revenues since 1982, CBO found that the mean absolute error—that is, the average of all errors without regard to whether they are positive or negative—was 2.2 percent for forecasts for the current year, 5.0 percent for projections for the subsequent fiscal year, and 10.1 percent for projections for the sixth year of the projection period.

The extent to which the relatively small errors in projected receipts for 2018 and 2019 and the downward revisions to projected receipts over the following decade were influenced by the effects of the 2017 tax act’s being larger or smaller than CBO projected or by other factors is not known. Those revisions to projected receipts reflect various factors, including revised economic projections, changes in tax modeling methodologies, and the incorporation of recent data on tax collections. The revisions do not reflect an explicit reassessment of the effects of the 2017 tax act, but they may be influenced by how those effects have unfolded over the past two years. For example, although CBO has revised downward projected receipts for 2020 by $58 billion (or 1.6 percent), largely to reflect weakness in recent tax collections, the extent to which those lower-than-expected receipts reflect the effects of the 2017 tax act or unrelated underlying factors is not known.

The effect of the Tax Scam may be "not known", but what we can do is compare what the CBO thought we would see in April 2018, and what has happened since. And as you can see, corporate revenues in particular have dropped even further than they thought it would after the Tax Scam's giveaways took effect.

In fact, between income, payroll and corporate taxes, there was a gap of more than $60 billion in the recently-completed Fiscal Year. That would have taken the total cost of the Tax Scam to nearly $500 billion in the last 2 years. But the shortfall was reduced to $28 billion (and $464 billion total) due to a significant increase in tariffs and other revenues that wasn’t predicted at the time. And that choice has come with its own set of economic issues, along with farm subsidies that spent almost all of that extra tariff revenue.

The CBO adds that we still need more information to get a complete picture of the fiscal effects of the Tax Scam, as we still are sorting out the last details of the first year under the new law.

Although some preliminary information has become available from tax returns filed for the 2018 tax year—the first returns that reflect most of the changes made by the tax act—that information does not clearly indicate whether the tax act’s effects differed from those CBO estimated in April 2018. Indeed, tax returns for 2018 for those who received extensions were filed only within the past two weeks. Detailed information from 2018 tax returns is expected to become available in late 2020. Assessing the tax act’s effects on receipts will not be possible even then, however, because it is not possible to disentangle changes in revenues caused by the tax act from changes driven by other factors, such as the effects of trade barriers that might have reduced economic growth and thus held down tax receipts. CBO will continue to monitor data to assess the effects of the 2017 tax act and to update its projections of tax revenues under current law.

So stay tuned, as we might still see more effects of the GOP Tax Scam in next month's revenue figures. Given that it involves filing extensions of 2018 taxes, it might reduce the total cost, as it would make sense that many of the extenders would be people having to write their checks to the IRS after under-withholding due to Trump Admin policy. But whatever revenue that might be made up in October won't come close to the losses in revenues that we've seen in the first 21 months of the Tax Scam, and with the economy slowing in 2019, that gap might grow again as people adjust and file in this winter.

This week, the Federal Reserve is expected to cut its benchmark interest rate by another ¼ point, down to 1.5%-1.75%. That comes on top of the Fed injecting $120 billion into the economy in repurchase agreements to make sure banks have enough money to keep operating as normal.

This current round of monetary-policy easing was described as a mid-cycle adjustment by Fed Chairman Powell earlier this year, a strategy that has been implemented in the past to preempt slowdowns and this time is being used to combat the negative effects of a nasty China-U. S. trade conflict.

Experts say that a third cut matches the definition of a mid-cycle shift and could be justified as further insurance as a recession that appears to be emerging in Europe is creeping up on the U.S.

Keith Lerner, chief market strategist at SunTrust Advisory Services, pointed to a trio of rate cuts in 1995 and 1998 as parallels for the current monetary tactic.

“Actually, both 1995 (which Powell has often talked about in a favorable light) and 1998 both saw three 25 basis point rate cuts and then the Fed stopped; these are both largely looked at as mid-cycle adjustments or for insurance reasons, especially 1995,” the SunTrust strategist said.

The stock market has certainly gotten more Bubbly in recent weeks, in the hopes that lower interest rates and Trump-generated rumors about a truce in trade with China will keep the economy goosed for the near future.

But why would we believe that things will get better than we have today? On Monday, there was more evidence that the weakness in manufacturing and trade was continuing, if not getting worse. For example, while the country’s trade deficit for goods got smaller in September, it wasn’t for the “good reason”.

The international trade deficit was $70.4 billion in September, down $2.7 billion from $73.1 billion in August. Exports of goods for September were $135.9 billion, $2.2 billion less than August exports. Imports of goods for September were $206.3 billion, $4.9 billion less than August imports.

COMMENTS: “Results from the October 2019 NABE Business Conditions Survey show that the U.S. economy appears to be slowing, and respondents expect still slower growth over the next 12 months,” said NABE President Constance Hunter, CBE, chief economist, KPMG. “Many of the survey indicators in this report are at their lowest levels in several years. It is important to note, however, that all respondents still expect the current economic expansion to continue over the next 12 months. But, on balance, panelists expect slower growth than they did three months ago. After more than a year since the U.S. first imposed new tariffs on its trading partners, higher tariffs are disrupting business conditions, especially in the goods-producing sector. Two-thirds of respondents from that sector indicate that tariffs have had negative impacts on business conditions at their firms.”

“More panelists report falling sales and anemic profit margins at their firms over the past three months than in the previous survey,” added NABE Business Conditions Survey Chair Sam Kyei, CBE, chief economist, SAK Economics LLC. “Materials costs rose, on balance, at respondents’ firms, marking a 14th consecutive quarter of higher costs. However, price increases were only slightly more common than price cuts at respondents’ firms. Hiring was far less prevalent at panelists’ firms in the third quarter, as was wage and salary growth. A majority of respondents (53%) expects wages and salaries to be unchanged over the next three months.

“Capital spending decelerated among more surveyed firms in the third quarter than in the second,” continued Kyei. “Notably, fewer respondents reported increased capital spending on equipment and information technology at their firms than at any time in the past five years.

“Panelists have a less favorable view than in the previous survey of the Federal Reserve’s easing of its federal funds rate policy. Only 35% of respondents view the easing as favorable, compared to the 50% who held this view in July.”

This is why I find myself bewildered by Wall Street still jumping whenever the Trump Administration pulls a pump-and-dump scheme claims progress in trade discussions. The overall economy isn’t doing that well, and stopping the tariffs isn’t going to solve the problem of slower demand through weaker wage and job growth. Nor will it do much to spark a full-employment economy in a country that is demographically aging.

So pumping up the stock market through easy money seems to be a sure-fire way to make what might be a natural and light recession into something much worse when things officially decline. Greedheads and Trumpists may not mind it, but those of us outside of BubbleWorld should care a lot.

Sen. Ron Johnson met in July with a former Ukrainian diplomat who has circulated unproven claims that Ukrainian officials assisted Hillary Clinton’s 2016 presidential campaign, a previously unreported contact that underscores the GOP senator’s involvement in the unfolding narrative that triggered the impeachment inquiry of President Trump.

In an interview this past week, Andrii Telizhenko said he met with Johnson (Wis.) for at least 30 minutes on Capitol Hill and with Senate staff for five additional hours. He said discussions focused in part on “the DNC issue” — a reference to his unsubstantiated claim that the Democratic National Committee worked with the Ukrainian government in 2016 to gather incriminating information about then-Trump campaign chairman Paul Manafort. Telizhenko said he could not recall the date of the meeting, but a review of his Facebook page revealed a photo of him and Johnson posted on July 11.

A Wisconsin reference in the long-awaited Mueller report provides a glimpse into why Russians trying to help President Donald Trump win the 2016 election may have targeted the state.

Wisconsin and other Midwestern battleground states were discussed during an election briefing former Trump campaign chairman Paul Manafort gave to Konstantin Kilimnik, a business associate with ties to Russian intelligence, the report says.

"That briefing encompassed the campaign's messaging and its internal polling data," the report says. "It also included discussion of 'battleground' states, which Manafort identified as Michigan, Wisconsin, Pennsylvania and Minnesota." ….

Investigators found that some of Trump’s aides engaged in contacts with people linked to the Russian regime as the Kremlin was carrying out a wide-ranging effort to intervene in the election using hacked documents and phony social media campaigns, carried out because the Russian government believed it would benefit from Trump winning the election.

In addition to being a likely beneficiary of the Russian propaganda effort in 2016, the Washington Post article noted that Johnson holds positions in the Senate that allow him to know all about Russian/Ukrainian interference in elections. It also allows Russian Ronnie to decide what issues on election hacking should be looked at....and which ones won't be.

The senator’s committee assignments place him at the center of U.S.-Ukraine policymaking: Johnson is chairman of the Foreign Relations Subcommittee on Europe and Regional Security Cooperation and vice chair of the Senate Ukraine Caucus, a bipartisan group formed in 2015 to boost ties between Washington and Kyiv. He is also chairman of the Homeland Security Committee, a panel with investigative powers.

More significantly, testimony from two blockbuster witnesses in the impeachment probe place Johnson at episodes that will be critical in assessing whether Trump was withholding nearly $400 million in congressionally appropriated military aid to Ukraine in exchange for political favors. Ukrainian President Volodymyr Zelensky faced pressure to announce investigations into the Bidens and the debunked conspiracy theory that a hacked DNC server was taken to Ukraine in 2016 to hide evidence that it was that country, not Russia, that interfered in the presidential election.

Johnson’s knowledge of key events could make him a person of interest to House impeachment investigators, as well as complicate his role as a juror in a trial by the Senate, if one occurs. There are no rules forcing senators with possible conflicts of interest to recuse themselves during impeachment proceedings, and Johnson, through a spokesman, declined to comment on what he would do.

It seems like Russian Ronnie needs to make an appearance before Adam Schiff and other House investigators to explain what he knows, and why he continues to try to deflect from the Trumpian sketchiness that surrounds the 2016 and 2020 elections.

It’s time for the House and national media to fully expose this slug, and to put the pieces together on the amoral money-laundering that is part and parcel for GOP/NRA in both DC and Wisconsin. This goes well deeper than the White House, folks, and it wasn’t just Trump that benefitted from the Russian/NRA/GOP axis.

A common theme that's emerging in the corporate media in the health care debate is "Medicare for All is expensive. How will Dems pay for it? "

As an example, "left-leaning" Rick Newman examined Elizabeth Warren’s wide-ranging plans in Yahoo! Finance, and expressed alarm at “the staggering cost” of the major changes that Warren wants to put into place to unrig our economic system.

Altogether, the Massachusetts senator’s agenda would require $4.2 trillion per year in new federal spending, and a like amount in new taxes, if she paid for everything without issuing new debt. The federal government currently spends about $4.4 trillion per year, so Warren’s plans would nearly double federal spending.

The Treasury takes in about $3.4 trillion in tax revenue each year, so if Warren levied new taxes to pay for everything, federal taxation would rise by 124%. She could pay for some of her plans by issuing new debt instead of raising taxes, but with annual deficits close to $1 trillion already, that might be unwise.

Newman is using the “$3.4 trillion in tax revenue” and “$4.4 trillion in spending” that the US got in the 2019 Fiscal Year. However, this is a bad comparison.

1. Newman uses 2019 figures for tax revenues while using the 10-year (inflation-increased) average for Medicare for All. That’s not a fair figure, because as you’ll see below, the net cost the Urban Institute got for Medicare for All in 2020 was $2.7 trillion.

2. If you look at the Congressional Budget Office’s projections for the next 10 years, the correct numbers are $4.6 trillion in average tax revenue and $5.8 trillion per year in spending. So while implementing all of Warren’s plans would likely lead to a significant increase in government spending and taxes, it will not require doubling spending or taxes to do so.

3. Also worth noting – the added spending assumes other areas won’t have spending cuts, which seems unlikely in Warren presidency (particularly the military and Border Patrol, both of which have been massively beefed up under Trump).

Newman does note that Warren’s plans-to-date do account for the $800 billion a year in initiaitives that are outside of Medicare for All.

But that still leaves the largest blue circle on the right.

The biggest chunk of new spending in Warren’s agenda, by far, would be Medicare for all, the single-payer health plan she would impose to replace all private insurance. Warren explains how she would pay for all of her plans—except this one. With fellow Democratic candidates pressing her for details, Warren says she’ll provide financing options for Medicare for all soon.

A single-payer plan covering every American would cost about $3.4 trillion per year, according to the Urban Institute and other analysts. Again: that’s equal to all federal tax revenue in 2019. Warren says “costs” would go down for middle-class families under Medicare for all, because all care would be free and families would end up paying less in new taxes than they now pay for health care. But that doesn’t mean Americans would be comfortable with the tradeoffs.

I immediately questioned that figure to Newman on Twitter, claiming that this figure wasn’t accounting for the fact that Medicaid and Medicare would be absorbed into the new program. But I was mostly wrong about that, as the $3.4 billion is the EXTRA cost of Medicare for All on top of what we do today in those programs and other federal aid.

Fair enough, but let’s dig further into the Urban Institute report that Newman cites and see where this figure comes from. First off, the Urban Institute’s estimate comes from the widest-ranging type of single-payer you could have (reform 8 in a list of ways to expand medical coverage). All American residents (not just citizens) are covered, and a large range of services are covered.

Single-payer enhanced program covering all medically necessary health benefits (dental, vision, hearing, and nationally uniform home- and community-based LTSS), eliminating cost sharing, enrolling all US residents (including the undocumented population), maintaining Medicaid for institutionally based LTSS, and eliminating private health insurance coverage.

OK, so what would it cost and how much would it cover, using 2020 estimates?

Coverage. Reform 8 is the only one in this report that eliminates uninsurance among both the legally present and undocumented immigrant populations. This intent, clearly indicated as components in the most-discussed single-payer proposals,30 introduces some additional uncertainty into the estimates. For example, we do not attempt to estimate any potential effect of additional residency (legal or otherwise) or medical tourism that could result from the reforms.31 Nor do we estimate less than universal coverage among the undocumented population, some of whom might decline providing information to a government entity for fear of deportation. Thus, we estimate this single-payer program covers 331.5 million people (table 13), increasing minimum essential coverage by 34.6 million people compared with current law. The program eliminates all other forms of insurance coverage.

Health care spending. Net federal government health spending, accounting for savings from eliminating Medicare, Marketplace subsidies, the acute-care portion of Medicaid, and uncompensated care, as well as savings on other federal insurance programs, increases by $2.8 trillion in 2020. Offsetting increases in income tax revenue mean $2.7 trillion in additional federal revenue is needed to finance the new program.

The $157.6 billion income tax offset results from employers not getting a tax break due for providing health insurance, because that becomes superfluous when the “providing insurance” part is taken care of under Medicare for All.

But that $157.6 billion that business won’t get in tax breaks is small compared to savings that will come to them, consumers, and states under single-payer.

States’ health care spending decreases by $259.6 billion, accounting for continuing Medicaid spending on institutionally based LTSS and savings from eliminating Medicaid/CHIP acute care, other state-specific programs, and uncompensated care. Employer spending on health care decreases by $954.7 billion, and household spending falls by $886.5 billion. The only remaining household spending required is in the continuing Medicaid program for those using LTSS. Providers no longer face any uncompensated care because all care is financed through the federal government, reducing their aggregate spending by $24.1 billion

So that knocks off more than $2.1 billion of that $2.7 billion in 2020. Most of that $2.1 billion isn’t currently collected as “taxes”, but it sure takes money out of the pockets of people and businesses, which has a significant effect on our economy.

Even the Urban Institute followed up their single-payer analysis by noting that Newman’s alarmism about “$34 trillion in new taxes” is misleading. Because while the total amount of spending is higher, it’s nowhere close to that level.

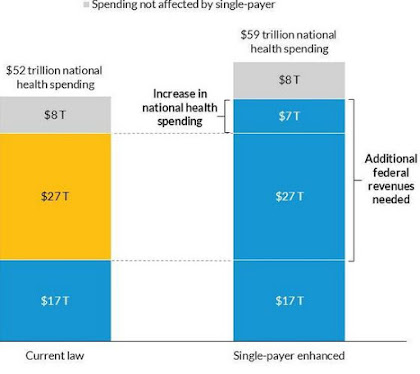

For this approach to reform, federal spending would increase by $34 trillion over 10 years, but health spending by individuals, employers, and state governments would decrease by $27 trillion, so national health spending would increase by $7 trillion over the same 10-year period, from $52 to $59 trillion.

The $8 trillion includes costs associated with an array of expenses, such as medical care for members of the military and their families while military members are deployed, services provided to foreign visitors, acute care provided to people living in institutions (e.g., prisons and nursing homes), and the value of new construction and equipment put in place by the medical sector. This spending also includes long-term services and supports by states and individuals that would continue under reform. For our purposes here, we refer to this $8 trillion in spending as “spending not affected by single-payer.”

The taller second bar shows that the total national spending under a single-payer program would be higher than under current law. The $17 trillion in federal spending under current law would be shifted to help fund the new program, and the federal government would take over the $27 trillion in current health care spending by employers, households, and state and local governments.

Fully funding a new single-payer program would require an additional $7 trillion in federal spending beyond that repurposed $44 trillion. The $8 trillion in spending not affected by the single-payer program would continue to be funded by a mix of government and private sources.

Thus, it is not appropriate to compare an estimated increase in federal spending of $34 trillion over 10 years with a current-law level of national health spending of $52 trillion over the same period and conclude these are savings in national health spending.

True, but there aren't "$3.4 trillion a year in extra costs" either, like Newman claimed.

Theoretically that middle $27 trillion (the $2.1 trillion + inflation over 10 years) the feds take on can be made up for with higher federal taxes or lower aids to states/corporations (to offset some of the savings they get) or other methods.

Does it mean Warren owes an explanation for the $700 billion a year that still needs to be account for? Maybe, but I’d also argue that the benefits of more security and a lack of “job lock” due to having health care be a right is well worth $40 a week to the typical American. In addition, the extra usage of medical services would likely raise GDP, which would have its own positive effect of raising tax revenue through economic activity.

I’ll also add that it’s funny how Republicans can throw $1.5 trillion down the tubes to a Tax Scam that has done nothing for most Americans, and "serious people" in our media never asked them in 2017 what program would have to be cut if/when a budget hole opened up. So if deficits are going to be huge as 2020 looms (not saying it doesn't matter, just saying if they're a given), isn't it better to have those deficits be a result of letting everyday Americans have more money in their pockets due to $0 in premiums and out-of-pocket expenses?

A little slamming of how insurers and drug companies screw over the average Joe/Jane wouldn’t be a bad move either. We used to not care so much about cost and what might happen to the corporate and comfortable when it came to making the country into a better place. Returning to that mentality would be the real way to MAGA.

A former Senator from Massachusetts understood that in 1961, and what better way to “assure the survival and success of liberty” than to stop having us be beholden to employers and/or a soulless insurance industry to have the basic security of health?

Maybe corporate media should talk about Medicare for All from that perspective on Sundays. After this message from Pfizer/Humana, of course.

Not long after Foxconn Technology Group announced plans to build a massive manufacturing facility in southeast Wisconsin, the tech giant began making promises to share its model for economic development across the entire state. But 18 months after purchasing its first building in downtown Milwaukee, there is little evidence that what Foxconn calls its innovation centers are moving forward.

In addition to Milwaukee, innovation centers have been announced in Green Bay, Eau Claire, Racine and Madison. Development directors in those cities say Foxconn now appears to be focused on its main manufacturing campus in Mount Pleasant.

The Eau Claire and Milwaukee buildings are still largely empty, the building Foxconn purchased on the Capitol Square in Madison last year hasn't had anything done to it, and Green Bay's alleged innovation center is also vacant.

Kevin Vonck, Green Bay’s development director, said early on Foxconn was meeting with contractors, but plans have been paused. The company is now planning to start interior construction in 2020, Vonck said.

"I think they are re-evaluating their strategy throughout the state and their focus is on southeastern Wisconsin," Vonck said. "They are also seeing how this location correlates with each of the innovation centers throughout the state."

When the Green Bay project was originally announced, Foxconn said it would open by late 2018. Vonck said he would like for it to move faster, but understands development of any kind has fits and starts.

But the news from the polls continued to be negative. The MU poll in March 2018 found that while 57 percent of registered voters statewide believed the Foxconn plant would benefit the greater Milwaukee area, only 25 percent felt the businesses where they live would benefit from the project. Fully 66 percent said their local businesses wouldn’t benefit.

Clearly Walker still needed help with this issue and Foxconn was soon riding to the rescue. In June Foxconn announced it would be buying a six-story building in Green Bay to create another “innovation center” which will employ more than 200 engineers. When this would happen wasn’t specified (“later this year”, the company said), but Gov. Walker was on hand to declare that this new center would extend Foxconn’s footprint to “northeastern Wisconsin.”

And Murphy saw what was coming for 2019.

No doubt there are potential employees and suppliers to be found in other parts of the state, but are we living in the age of plank roads and mule teams? Or are these potential partners too shy to use computers, email and cell phones or simply drive along those highway connections to Foxconn’s massive Racine campus that we taxpayers are financing. Why must the company instead create satellite connections all over Wisconsin in order to coax these elusive workers and companies from getting aboard the gravy train of the most publicly subsidized foreign company in American history?

Given the massive subsidy Foxconn is getting, it can probably afford to throw a little money at Eau Claire and Green Bay, even if those satellite centers are completely unnecessary. And Foxconn has every incentive to ensure that Walker wins reelection, given that all eight Democratic candidates for governor have condemned the deal and one, Matt Flynn, has promised to fight the deal in court. Foxconn, moreover, has a long history of backing out of projects it announces. If it could back out of deals in India, Vietnam, Brazil and Pennsylvania, why can’t it walk away from Eau Claire and Green Bay? It can merely explain, a couple months after the November election, that economic conditions have changed, or that it is having no problem getting the suppliers and employees it needs for its Racine plant, and so it won’t need those political outposts — sorry, innovation centers — that helped reelect their generous benefactor.

It's been a common theme for us liberals in the Age of Fitzwalkerstan.

Beyond the halted innovation centers, Foxconn’s general Wisconsin plans are similarly in flux. The company announced a partnership in September with an automated coffee kiosk company to help manufacture its product domestically, with plans to add the coffee kiosk to its manufacturing contracts for the planned Mount Pleasant factory.

But the factory doesn’t exist yet. The company is now aiming to open it in 2020 after repeatedly shifting its deadlines. It’s also reduced the planned number of jobs and the size of the factory from the original 13,000 jobs and 20 million square feet to a 1,500-employee, 1-million-square foot facility that will no longer produce the promised big-screen LCD TVs that were part of the initial contract. Earlier this month, the company announced, scrapped, and then re-announced plans to build a giant, nine-story glass orb that would serve as a data center.

So it's back...for now.

So two years after people were driven off their land and state and local taxpayers have shelled out more than $1 billion to fix up roads and other infrastructure in Racine County, we only have a handful of jobs, and no long-term idea what's going to happen at Foxconn.

Oh, but don't you worry, because a day after that WPR article appeared showing that the "innovation centers" were empty BS, Foxconn claimed it was going to fix up its Racine Innovation Center.

The City of Racine issued a permit to Foxconn Technology Group on Thursday for remodeling in a building the company has said will host one of its "innovation centers."

Foxconn filed an application for the permit Tuesday, a city spokesman said.

The plans call for building out a vacant area of the first floor of the building at 1 Main St., which Foxconn bought early this year for $6.25 million. The project would include construction of a conference/training space, a reception area, a small office and restrooms.

The space to be remodeled covers 1,451 square feet, the plans indicate. A little more than a year ago, Foxconn had announced it wanted proposals to remodel a 20,500-square-foot area. The firm said then that its goal was "to occupy the finished space in January 2019, or as soon as possible."

Finished in January 2019, eh? Think they missed the deadline on that one.

Tamarine Cornelius of Kids Forward said it well on how much of a missed opportunity this state has had because Scott Walker and Donald Trump were so desperate to get headlines as "job creators."

Think about how much time, money, and effort we've spent on Foxconn that we could have spent helping businesses grow and thrive. A lesson to other states, I hope. https://t.co/IqJRMKMM8H

Manufacturing sector business conditions continued to recover in October, as signalled by a rise in the IHS Markit Flash U.S. Manufacturing Purchasing Managers’ Index™ (PMI™ ) 1 to 51.5, up from 51.1 in September. The rate of improvement was the fastest for six months, helped by stronger growth of output, new orders and employment.

October data also pointed to an increase in new export sales for the first time in four months. Stronger demand encouraged a marginal rebound in input buying, but inventory volumes were depleted again.

But if manufacturing slightly picked up in October, it’s still from a lowered level in September. That was reiterated again with a Commerce Department report showing manufacturers’ orders and shipments both declined last month, including a sizable drop in new orders.

New Orders

New orders for manufactured durable goods in September decreased $2.8 billion or 1.1 percent to $248.2 billion, the U.S. Census Bureau announced today. This decrease, down following three consecutive monthly increases, followed a 0.3 percent August increase. Excluding transportation, new orders decreased 0.3 percent. Excluding defense, new orders decreased 1.2 percent. Transportation equipment, also down following three consecutive monthly increases, led the decrease, $2.3 billion or 2.7 percent to $84.5 billion.

Shipments

Shipments of manufactured durable goods in September, down three consecutive months, decreased $1.0 billion or 0.4 percent to $252.5 billion. This followed a 0.1 percent August decrease. Transportation equipment, also down three consecutive months, drove the decrease, $1.0 billion or 1.2 percent to $84.6 billion.

In addition, new orders for last month were 4% behind where we were in September 2018. That’s a bad harbinger for future growth, if demand has declined.

And the other problem is on the other end of the supply line, as there are more items on shelves, and fewer waiting to go out.

Unfilled Orders

Unfilled orders for manufactured durable goods in September, down following two consecutive monthly increases, decreased less than $0.1 billion or virtually unchanged to $1,163.5 billion. This followed a 0.2 percent August increase. Fabricated metal products, down following three consecutive monthly increases, drove the decrease, $0.1 billion or 0.1 percent to $87.0 billion.

Inventories

Inventories of manufactured durable goods in September, up fourteen of the last fifteen months, increased $2.1 billion or 0.5 percent to $430.3 billion. This followed a 0.2 percent August increase. Transportation equipment, also up fourteen of the last fifteen months, led the increase, $2.1 billion or 1.4 percent to $145.3 billion.

The year-over-year numbers are also bad in these stats, with unfilled orders dropping by more than $20 billion from September 2018 (-1.8%), and inventories are up $19.5 billion under the last 12 months (+4.75%).

In addition, we found out yesterday that new homes sales dropped back down in September. And while the Federal Reserve of Atlanta still keeps projected GDP growth for Q3 at 1.8%, it’s in a slightly different form from the 1.8% they projected nearly 2 weeks ago.

Changes in contributions to Q3 GDP, Atlanta Fed

Consumption +0.06%

Equipment -0.07%

Nonresidential structures -0.02%

Residential homes +0.02%

Net Exports -0.01%

Inventories +0.03%

Looking ahead, the Chief Economist of IHS Markit (who puts together the PMI survey) said things would continue to sputter to round out 2019.

“Despite business activity lifting from recent lows, the survey data point to annualized GDP growth of just under 1.5% at the start of the fourth quarter, and a near-stalling of new order growth to the lowest for a decade suggests that risks are tilted toward growth remaining below trend in coming months.

“An increased rate of job culling adds to the gloomy picture, with jobs being lost among surveyed companies at a rate not seen since 2009. At current levels, the survey’s employment gauge indicates non-farm payroll growth slipping below 100,000.

“The overall subdued picture reflects a spreading of economic weakness from manufacturing to services, but encouragingly we are now seeing some signs of manufacturing pulling out of its downturn, in part driven by a return to growth for exports and improved sentiment about the year ahead, linked to hopes that trade war tensions are starting to ease.

And yet Wall Street has been on the rise in the last 2 weeks, likely because profit growth has been surprisingly well. But in the real economy, there are signs that the slower growth isn’t just at the factories these days, and the 4th Quarter will likely tell us if it reverses, or speeds toward a 2020 decline.

A. Wayne Johnson made the statement was a Republican appointed by Education Secretary Betsy DeVos, and said the current system is “fundamentally broken” with large amounts of defaults and financially hamstrung graduates.

Indeed, five years into repayment, half of student loan borrowers haven’t paid even $1 toward their debt’s principal, according to the Education Department’s own data. And 40% of student loan borrowers could default by 2023, according to an analysis by the Brookings Institution.

“We run through the process of putting this debt burden on somebody … but it rides on their credit files — it rides on their back — for decades,” Johnson, who wrote his dissertation at Mercer University on student debt, told the Journal.

“The time has come for us to end and stop the insanity,” he added.

Johnson proposes forgiving $50,000 in student debt for all borrowers, about $925 billion, according to the newspaper. For people who’ve already repaid their debt, he suggests offering them a $50,000 tax credit. The plan would be paid for with a 1% tax on corporate earnings.

At the same time, Johnson announced he’d be running for an open Senate seat in Georgia.

And a “1% tax on corporate earnings” would be a mere fraction of what corporations got as part of the GOP Tax Scam that was passed in late 2017. Just sayin'.

This graphic from CNBC gives you an idea about student loan debt has kept climbing in the last 15 years. And notice how people over 40 especially have had larger amounts of debt in recent years.

A smaller plan would write off less debt, but would also potentially have big benefits, given the large number of people with relatively small debt loads but are still paying (or not able to pay).

Cancelling $10,000 of every federal student-loan borrower’s debt would wipe out the federal student loans for about 40% of borrowers who aren’t in a grace period or aren’t in school, according to an analysis from the Center for Responsible Lending, a consumer advocacy group.

The $10,000 benefit would also totally cancel the federal student-loan debt of 61% of the more than 7 million borrowers who are in default on their loans, the analysis shows.

Even borrowers with some debt remaining would receive a relatively significant benefit, according to CRL. Borrowers in repayment with debt levels in the third quintile would see their balance drop by 80%, borrowers in the fourth quintile would have 42% of their debt cancelled and borrowers with the highest debt levels would see 17% wiped away.

In addition, a 1990s tax provision intended to help students that have taken on loans now seems to be backfiring. The IRS notes that student loan interest deduction can get someone to write off up to $2,500 in income, IF they are below certain income thresholds.

For 2018, the amount of your student loan interest deduction is gradually reduced (phased out) if your MAGI [Modified Adjusted Gross Income] is between $65,000 and $80,000 ($135,000 and $165,000 if you file a joint return). You can’t claim the deduction if your MAGI is $80,000 or more ($165,000 or more if you file a joint return).

Here’s the Catch-22 – if you got a good-paying job after taking out a loan to get more schooling (a gap that has grown significantly in the last 20 years), you may well not get that deduction. This comes straight from last week’s release from the Bureau of Labor Statistics.

Median annual income (using weekly wage) by education, US

Bachelor’s Degree $66,612

Advanced Degree $81,068

You can see the median person with a Master’s is already above the limit for writing off the student loan interest, and a person with a Bachelor’s that’s in the middle of the upper half for income also gets nothing.

One could say “Well, you’re making a lot of money, so what’s the problem?” Except the loans that paved the way to the higher incomes now are preventing a higher standard of living because more of that money has to be used to pay off the loans.

Even if they don’t want to entirely remove student loan debt like Johnson or Elizabeth Warren or Bernie Sanders do, it seems like a logical move for Dems (who get the majority of votes of people with Bachelor’s and Master’s degrees) to use next month’s budget debate to reward those who took on loans to improve their education. They can do so by raising the student loan interest cap to $100,000 single and $200,000 married/joint filer and/or raising the $2,500 limit on student loan interest (which hasn’t gone up in years). It would be a relatively small price tag, and could be easily paid for by bumping up some of the corporate/rich giveaways in the GOP Tax Scam.

In addition, a double-whammy has hit many people with educations and homes since the end of 2017. A recent ProPublica analysis went into how the GOP’s Tax Scam has hurt homeowners in many states (including Wisconsin), because of the limitation on State and Local Taxes (SALT), which is reducing what used to be a big incentive to own a house.

The SALT deduction was capped at $10,000 starting last year, is the same for single and married joint filers (VERY stupid), and many people with high education and higher earnings go over that total. Here was a map that showed which areas of America were most susceptible to hitting against the SALT cap.

On top of that, the Tax Scam raised the standard deduction to $12,000 for a single person and $24,000 for a married couple, which made married couples especially worse off if they took the SALT deduction, as many don’t have $14,000 in other deductions to add in.

As a result, those people got zero in deductions for both SALT and mortgage interest for both this year and the foreseeable future, which makes home ownership less worthwhile. Moody’s chief economist Mark Zandi told ProPublica that the results of the Tax Scam likely has put a lid on home values.

Zandi says that because of the 2017 tax law, U.S. house prices overall are about 4% lower than they’d otherwise be. The next question is how many dollars of lost home value that 4% translates into. That isn’t so hard to figure out if you get your hands on the right numbers….

Here’s how it works. Zandi took what financial techies call the “present value” of the property tax and mortgage interest deductions that homeowners will lose over seven years (the average duration of a mortgage) because of changes in the tax law and subtracted it from the value of the typical house. That results in a 3% decline in national home values below what they would otherwise be.

The remaining one percentage point of value shrinkage, Zandi says, comes from the higher interest rates that he says will result from the higher federal budget deficits caused by the tax bill. He estimates that rates on 10-year Treasury notes, a key benchmark for mortgage rates, will be 0.2% higher than they would otherwise be, which in turn will make mortgage rates 0.2% higher.

And that effect is notably higher in places in that chart in the darker blue….which often corresponds with places that have a higher percentage of high-educated people. Granted, we haven't seen that much in Wisconsin yet (our bigger problem is housing affordability, especially in Dane County), but if things go bad, the lack of write-offs might speed that decline.

I know the “upper-middle class educated person in a big metro area” isn’t a sympathetic group in 2019 America. But they’re also caught in a significant squeeze these days, which helps to explain why so many of us with decent incomes feel like we’re not much better off despite an allegedly strong economy. Because the costs that have been taken on in order to get to that higher level still are being paid for, while ending up on the wrong end of much of our flawed tax system. Meanwhile, the super-rich have gotten more tax breaks, and the poor (rightfully) got somewhat of an expanded safety net.

A big reason Dems controlled the House of Representatives after the 2018 elections was through gains in places that got hit the worst by the SALT cap (6 in California, 4 in New Jersey, 3 in New York, 3 in Virginia, and 2 in Illinois). It seems that fixing that flaw in tax policy and giving more assistance in dealing with student loan debt wouldn’t just be good economic policy, it also would lead to even more Dem wins in 2020.

Reflecting state and national demographic trends, the University of Wisconsin System’s preliminary enrollment for fall 2019 is 167,186 students, an overall 2.6 percent decline from last year.

Nationally, higher education enrollments are down. These modest enrollment reductions are not unique to the UW System amid trends of fewer high school graduates and low unemployment rates in a strong economy….

Overall, preliminary fall 2019 enrollment in the UW System declined by 4,450 students compared to 2018.

This is a problem because with no additional funds to pay for a tuition freeze, the declining enrollment means campuses will be limited in the amount of resources that it can use.

On the other side, student fees barely increased, and room and board revenues declined for 2019-20. The “Other Fees” listed did go up, which are basically fees for applications and placement tests, and special programs and courses that go beyond your typical tuition.

It's worth adding that Madison has more opportunities to receive funds from those “Other Fees” than the typical UW System school. And the two-sided story continues when you go back to the enrollment figures, and realize that there would be a much larger drop System-wide if you removed the flagship school. And the former UW Colleges (now known as “branch campuses”) are especially losing out.

UW enrollment change 2019-20

UW-Madison +879 (+2.0%)

Other UW main campuses -2,874 (-2.4%)

UW “branch campuses” -2,455 (-25.2%)

Which illustrates the folly of a decision System President Ray Cross made 2 years when he and the Walker-stacked Board of Regents unilaterally changed how the Colleges were going to operate. The enrollment decline led the college dropout that chairs the Assembly’s Colleges and Universities Committee to hint at an even bigger change in the future, as part of an alarming report by Wisconsin Public Radio.

Declining enrollment at the former UW Colleges was cited as a main driver of the restructuring when Cross announced in October 2017 that the state's two-year colleges would be merged with its four-year universities. At the time enrollment at all UW College campuses had already dropped by around 19 percent compared to 2010 figures.

State Rep. Dave Murphy, R-Greenville, advocated for the UW restructuring. Murphy said there were bright spots in the enrollment data with enrollments going up at UW-Madison, UW-Green Bay And UW-Superior, though he said, "Obviously the two-year campuses are really struggling."

"And there are campuses that may have to be closed in the future, and I think you need to keep it in mind," Murphy said. "Is it a little premature? Maybe, that we need to hold off and continue to look at it a little bit. But I think some time in the very near future some tough decisions might have to be made on those things."

Sounds like a way to make the 2-year Colleges and non-Madison campuses spiral downward through strangulation of resources, and require changes as a result of this dysfunction. Just the way the ALEC Crew likes it.

These enrollment and outside revenue figures reiterate how Madison is able to get more tuition revenue through more students, and more resources outside of tuition and state aid. Seems like all the more reason to break off Bucky from the rest of the system when it comes to state aid. This would be designed as a win-win where Madison is freed up from the handcuffs of regressive GOPs in the Legislature, and the other UW campuses that are struggling to stay afloat (especially the 2-year Colleges) get more state funds to protect against enrollment fluctuations that make it harder to get by.

Today had the release of the latest Marquette Law School Poll. And the typical summary of it sounded something like this.

A narrow majority of Wisconsinites oppose impeachment of President Donald Trump, though support has grown since earlier this year, according to the latest Marquette Law School Poll.

The poll, conducted Oct. 13-17 among 799 registered voters, found 51% of respondents said the president should not be impeached and removed from office, while 44% said he should be impeached. The poll has a margin of error of +/-4.2 percentage points.

In addition, the poll, the first since Congress began impeachment inquiry hearings regarding Trump's conduct related to Ukraine, found 49% of respondents said they don't believe there is enough information to support impeachment proceedings, compared to 46% who said there is enough....

As far as Trump’s job approval, 46% of respondents approve of the job he's doing as president, while 51% said they disapprove.

Trump’s job approval numbers have been relatively consistent throughout the year. He had a 44% approval rating in January, compared with a 52% disapproval rating.

That was a bit surprising, given recent events and Trump's clear slide in the polls. But once you dig into the MU poll a bit it makes sense.

Ideology Conservative

MU Law Poll 40.6%

2016 exit poll 34%

Moderate

MU Law Poll 33.8%

2016 exit poll 40%

Liberal

MU Law Poll 25.6%

2016 exit poll 25%

And why is this is a big deal? Because while conservatives overwhelmingly approved of Trump and didn't want impeachment, moderates disapproved of Trump 33-61, favored impeachment hearings 53-39, and even backed impeachment AND REMOVAL 47-46.

If the ideological demos matched the 2016 exit polls, here’s what you'd get.

MU Law Poll with 2016 exit poll ideology Trump approval

From 46-51 to 43-54

Have impeachment hearings

From 46-49 to 48-46

Impeachment + removal

From 44-51 to 46-48

That's not a lot of points, but would likely cause a major change in perception. Especially if the headline was "Trump approval falls and impeachment hearings favored."

Gee golly willikers, that's what the people told us.

Also worth noting is the Age disparity.

Age 18-44

MU Law Poll 34%

2016 exit poll 40%

2018 Census figures 44%

Age 45+

MU Law Poll 66%

2016 exit poll 60%

2018 Census figures 56%

And that's another key split in these questions.

Trump approval

18-44 -15

45+ -0.1

Have impeachment hearings

18-44 +2.1

45+ -5.8

Impeachment + removal

18-44 +2.8

45+ -12.3

That's not a misprint, younger voters want Trump removed even more than they want impeachment hearings themselves!

So if people under 45 were projected to turn out as much as people 45+ turn out, the Dem candidates wouldn't be up a few points in Wisconsin, but more like 8-10. And impeachment would be nearly at 50% already. Demos matter. And if only old people respond to politics in Wisconsin, GOPs do better. While if younger people show up, Dems win, often by a sizable amount.

Of course, this poll was taken between 6 and 10 days ago, and a whole lot has emerged since then, with most of it making impeachment more likely, and Trump's electoral prospects worse. But that's not going to stop the media from saying Wisconsin is still a toss-up state for now, based on a typical elderly and conservative Marquette Poll.