Based on preliminary collections information through December, 2022, individual income tax revenues for the current fiscal year are 12.9% lower than such revenues through the same period in 2021. This is primarily due to decreased withholding collections following the withholding table update that took effect January 1, 2022. However, individual income tax revenues are expected to increase at a rate of 21.1% over the next six months relative to the same period a year prior. The primary factor for this estimated revenue increase is an expected decline in refunds paid to taxpayers in 2022-23 relative to 2021-22. The income tax rate reduction included in 2021 Act 58, which took effect beginning in tax year 2021, caused refunds to spike when taxpayers filed their corresponding income tax returns in 2021-22. However, because the income tax withholding tables were later updated beginning January 1, 2022, to reflect the rates, brackets, and standard deduction in effect for current law, the amounts withheld from taxpayers during tax year 2022 incorporated the Act 58 rate reduction for the first time. As a result, when taxpayers file the corresponding returns in Spring of 2023, their refund amounts will be lower (all else equal) than the refunds they would have received had the withholding tables not been updated.So February is the first month where you will generally see those lower refunds, and March and April should repeat those trends on a larger dollar amount.

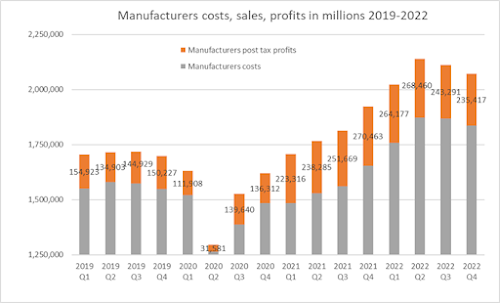

U.S. manufacturing corporations' seasonally adjusted after-tax profits in the fourth quarter of 2022 totaled $235.4 billion, down $7.9 (±2.8) billion from the after-tax profits of $243.3 billion recorded in the third quarter of 2022, and down $35.0 (±1.5) billion from the after-tax profits of $270.5 billion recorded in the fourth quarter of 2021. Seasonally adjusted sales for the quarter totaled $2,072.3 billion, not statistically different from the $2,111.3 billion in the third quarter of 2022, but up $148.4 (±28.3) billion from the $1,923.9 billion recorded in the fourth quarter of 2021.You can see that dollar amount of sales went up in 2022, but profits went down, which indicates that higher costs hit manufacturers last year. But what's not mentioned is that 2021 featured an 80% increase in post-tax profits from the end of 2019 to the 3end of 2021. and manufacturers were still in much better shape at the end of last year than they were in the pre-COVID era.

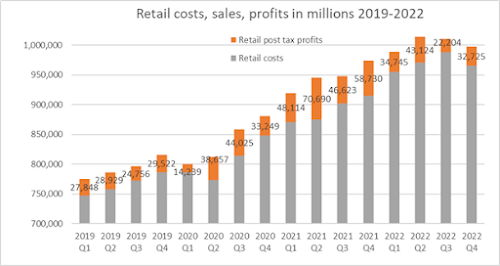

So let's not kid, even if the profits of these businesses were declining in 2022, they're coming off ridiculous highs from 2021. Manufacturers (especially) are doing just fine these days, but retailers are seeing some stresses. The positive in both of these things is that workers seem to have received a small share of the higher profits of 2021, but "inflation" still has been a nice boon to corporate profits in the last two years, and we will likely see more evidence of that when the Bureau of Labor Statistics releases its year-end info on all corporate profits later this week.The company is using the boost in revenue to lavish its investors and executives.

— More Perfect Union (@MorePerfectUS) March 23, 2023

General Mills has already spent $1.1 billion on buying back their own stock.

Oh joy! More racist BS crime ads from an organization that really doesn't care about crime issues, in an attempt to elect someone to a Supreme Court that doesn't hold criminal trials. And before some GOP hack chimes in with "But....Janet has so much money from donations!" - We can track where all of those donations to Protasiewicz came from, and who ponied up the money. WMC members don't have the guts to allow us to know the same about them.WMC Issues Mobilization today booked another $1.1M in broadcast TV ad spending

— Medium Buying (@MediumBuying) March 24, 2023

That brings their total TV/radio ad spending in the general election to more than $5.1M

WMC also hides the names of their member businesses and localThey exist for the purpose of laundering donations to WisGOP through a 501c6, so you can take a business deduction of your taxes and not have to comply with public disclosure requirements.

— Michael Bradley 🍕 (@MikeBradleyMKE) March 25, 2023

Wisconsin Manufacturers & Commerce (WMC) – the state’s largest and most influential business association – elected Kwik Trip Vice President Steve Loehr as Chairman of its Board of Directors on Thursday. Loehr will serve a two-year term and has been an active member of the Board since 2015. “WMC is an effective advocate for the business community and a respected thought leader on Wisconsin’s economy,” said Loehr. “I have been honored to serve on the Board and look forward to continuing to bring our state’s business leaders together to continue our work to make Wisconsin the most competitive state in the nation.” Waupaca Foundry, Inc. President, COO & CEO Mike Nikolai was also elected to a two-year term as Vice Chairman, while Teel Plastics, Inc. Chairman & CEO Jay Smith assumed the role of Immediate Past Chairman. Reelected to their posts as officers of the WMC Board are Gina Peter, an Executive Vice President at Wells Fargo Bank and Barbara Nick, President & CEO of Dairyland Power Cooperative, who will serve as Treasurer and Secretary respectively.Spend or boycott as appropriate, folks. Especially when the WMC lowlifes decide that being puppetmasters of power is more important than not having a state that treats women as second-class citizens or has free and fair elections with a representative Legislature.

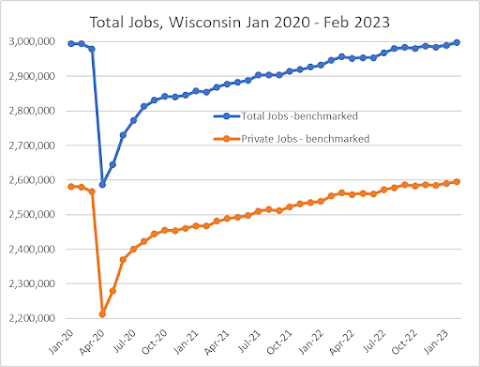

The Department of Workforce Development (DWD) [on Thursday] released the U.S. Bureau of Labor Statistics (BLS) preliminary employment estimates for the month of February 2023, which showed Wisconsin's seasonally adjusted unemployment rate dropped to a record low of 2.7%. In addition, total seasonally adjusted nonfarm jobs increased 7,500 over the month of February and 50,300 year-over-year to hit a new record high of 2,997,400. The total jobs number puts the state 3,400 jobs above pre-COVID-19 peaks.That’s great to hear, especially following recent reports of increased layoffs being announced by state companies in 2023 (which I’ll get back to in a bit). As the report indicates, Wisconsin now has finally passed the pre-COVID job levels slightly more than 3 years after that peak was hit in January 2020.

And if you watched the CNBC video, you'll notice that stocks also ticked up a bit after thre Fed's decision and Chairman Powell's press conference, as they figured things were steady enough, and only one more rate hike was priced in. But then something else happened after Powell spoke.Federal Reserve 'dot plot' shows interest rates peaking at 5.1% in 2023 https://t.co/V71uSfx9kf

— Yahoo Finance (@YahooFinance) March 22, 2023

by @alliecanal8193 pic.twitter.com/OkQQXkfp4o

And that something came in statements US Treasury Secretary Janet Yellen gave to a Senate committee, indicating that the Biden Administration would not bail out all bank depositors on their alone.Dow Jones fell down 500+ points in the last one hour trading session. pic.twitter.com/jsSRNdXCGS

— Asif Momin (@Asifmominblr) March 22, 2023

Some banking groups have urged the Biden administration and the Federal Deposit Insurance Corp (FDIC) to temporarily guarantee all U.S. bank deposits, a move they say will help quell a crisis of confidence after the failure of Silicon Valley Bank and Signature Bank. Reuters reported on Tuesday that government officials discussed the idea of raising the $250,000 insurance limit per depositor without congressional approval following the SVB and Signature closures. Yellen said she believed it was "worthwhile" for Congress to look at changes to FDIC deposit insurance, but declined to say what changes she thought were warranted. But when asked whether insuring all U.S. deposits required congressional approval, Yellen said she was not considering such a move and was reviewing banking risks on a case-by-case basis. "I have not considered or discussed anything having to do with blanket insurance or guarantees of deposits," she said.And Wall Street threw a tantrum, causing the big losses. For the record, I think that the $250,000 limits of FDIC insurance are probably outdated, and I think it would be a great idea for Congress to raise the fees banks pay to the Treasury in order to raise those limits. Which seems to be what they are going to try to do.

Senate Banking Committee chair @SenSherrodBrown says prospects are improving for legislation lifting the Federal Deposit Insurance Corp. cap, as senators discuss ideas ahead of a hearing on the failures of Silicon Valley Bank and Signature Bank. https://t.co/oNuab5JtUt

— Scott Suttell (@ssuttell) March 22, 2023

"There seems to be more commonality about what to do with FDIC than there was four or five days ago," the Cleveland Democrat told reporters Tuesday evening, March 21. "By our hearing next week, we may have some clarifying thoughts that there can be some consensus." The Banking Committee is scheduled to hear from FDIC chair Martin Gruenberg, Fed vice chair for supervision Michael Barr and Nellie Liang, the Treasury undersecretary for domestic finance..... "We'll examine deposit insurance coverage issues. We'll look at the role of social media. We'll consider legislation to strengthen guardrails and I'll continue pressing regulators to do a full review of those two bank failures and what is happening across the country," Brown said. "I think we could find some bipartisan solutions, perhaps on FDIC changes." Brown said Tuesday that proposals include raising the insurance cap, eliminating the cap permanently or temporarily, and creating a different insurance category for businesses. The brunt of any additional costs would have to be paid for "by the big guys," Brown said, meaning larger banks and larger depositors.But Wall Streeters want their bailout now, dammit! And to keep their low-rate coacine party as soon as they can. While I also think rates are too high, my reasons are because the Fed shouldn't stop what's a very good economy in the real America, and inflation has been on the wane for 8 months, to the point that real short-term rates are very high these days. I would hope the Fed goes on pause with its next meeting in May, particularly as oil prices have fallen to their lowest levels since 2021, and as food prices are finally moderating. To me, it's more important to keep the strong jobs market rolling along than in caring whether inflation is at 2% or 4%. Especially when interest rates are now at 5%

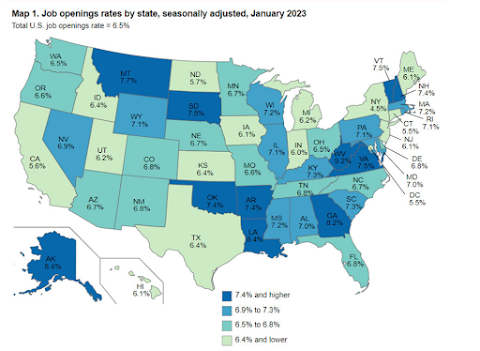

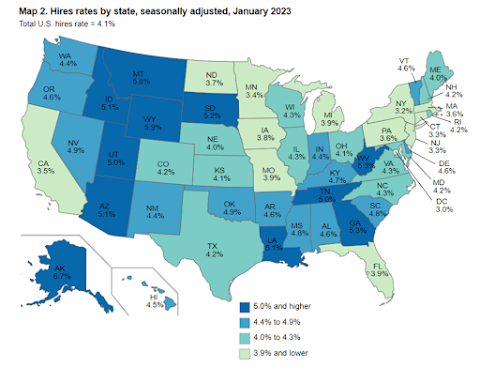

Over the first two and a half months of 2023, the Wisconsin Department of Workforce Development has seen an increase in layoff notices compared to the same period last year. So far, 1,963 workers have been affected this year. That’s more than half of the 3,821 total employees affected by layoffs in all of 2022. But the most recent unemployment data shows Wisconsin’s unemployment rate remained low at 2.9 percent in January — better than the 3.4 percent national rate that month — according to state Department of Workforce Development, or DWD.That seems like a big deal, and it’s within 10% of the total number of people involved in layoff notices for all of 2021. The rate of layoffs in 2023 is more in line with what we saw in the pre-pandemic year of 2019, when more than 8,500 workers were affected (granted, over ¼ of 2019’s layoffs came from Wisconsin-based Shopko, which went belly-up that year and closed all of its department stores). However, I also see some caveats with the 2023 layoff numbers. Nearly 1/5 of the losses are duet to Marshfield Clinic transitioning 377 workers to its Family Health Center spinoff, which starts on April 1 with no net jobs lost in the process. That’s not to say that Marshfield Clinic is doing fine, as it recently announced that 222 of its workers will lose their jobs in May across several locations in the state. Similarly, even though Yellow Corp. is closing their freight terminal on the South Side of Milwaukee, the company says it plans to move most (if not all) of those 189 jobs to its other facility in nearby Oak Creek. So while that’s an annoying disruption, it shouldn’t cause much economic damage to workers or the state in general. But that doesn’t mean there’s nothing to worry about. In addition to the Marshfield Clinic reductions, Hutchinson Technology in Eau Claire says it will lay off more than half of their 425 employees in the coming weeks and months, and triple-digit losses at Briggs and Stratton in Wauwatosa, Hubbell Gas Utility Solutions, and Biery Cheese in Plover are going to hit in March and April. Of course, if job openings remain high and hiring stays strong in Wisconsin, the higher number of layoffs won’t be as much of a harm. And we know that as of January, Wisconsin’s job market was going very well. The recent state-level JOLTS report says that Wisconsin started off 2023 with the highest level of job openings (as % of total jobs) in the Midwest, and the second-highest rate of hires.

Credit Suisse confirmed in February that clients had pulled 110 billion Swiss francs ($119 billion) of funds in the fourth quarter while the bank suffered its biggest annual loss of 7.29 billion Swiss francs since the financial crisis. In December, Credit Suisse had tapped investors for 4 billion Swiss francs. On Wednesday, Saudi National Bank, the bank's top backer, told reporters it could not give more money to the bank as it was constrained by regulatory hurdles, while saying it was happy with the bank's turnaround plan. Credit Suisse shares have lost more than 75% of their value over the past twelve months.And now we have reports of Deutsche Bank circling the withered body of Credit Suisse to bail it out and take those accounts. Likewise, isn't it funny how GOP mega-donor/overall scumbag Peter Thiel led a run on Silicon Valley Bank by telling the companies he invested in to get out of the bank a couple of weeks ago.

Thiel's Founders Fund is thought to have propped up several startups that banked with SVB, which provided banking for nearly half of all US venture-backed startups, per its website. The fund had also called for its startups to withdraw their funds from the bank as well. Bloomberg reported that VC funds Coatue Management, Union Square Ventures, and Founder Collective had all told their portfolio companies to pull their funds from SVB.If I was a conspriatorial-type person, I'd almost say that Thiel would be fine with trying to cause chaos in the economy to hurt Joe Biden and grab more power for oligarchs like himself. Especially when former US Labor Secretary Robert Reich reminds us of what Thiel has previously said and done.

Peter Thiel, the billionaire tech financier who is among those leading the charge, once wrote, “I no longer believe that freedom and democracy are compatible.” Thiel is using his fortune to squelch democracy. He donated $15m to the successful Republican Ohio senatorial primary campaign of JD Vance, who alleges that the 2020 election was stolen and that Biden’s immigration policy has meant “more Democrat voters pouring into this country.” Thiel has donated at least $10m to the Arizona Republican primary race of Blake Masters, who also claims Trump won the 2020 election and admires Lee Kuan Yew, the authoritarian founder of modern Singapore... Thiel and his fellow billionaires in the anti-democracy movement don’t want to conserve much of anything – at least not anything that occurred after the 1920s, which includes Social Security, civil rights, and even women’s right to vote. As Thiel wrote:Remember what happened to the economy at the end of the Gilded 1920s, a time when "real [male] leaders and optimistic job creators" controlled everything? It wasn't good. Then add in the reality that the Federal Reserve kept interest rates near 0% for 2 years, even as the economy had picked up and the Biden/Dems in charge of DC had put in massive stimulus to bring the country back from its COVID-related doldrums. Tech bros used the rock-bottom interest rates to borrow at ridiculously low levels, and then as their products became less needed as the COVID pandemic faded, and the "optimism" about their "disruptions" didn't work out, they have little money coming in to justify the inflated stock prices. Which is why I like to look at the S&P price-to-SALES ration to get insight on legitimate stock valuations. And it looks like a deflated Bubble over the last year.The 1920s were the last decade in American history during which one could be genuinely optimistic about politics. Since 1920, the vast increase in welfare beneficiaries and the extension of the franchise to women – two constituencies that are notoriously tough for libertarians – have rendered the notion of “capitalist democracy” into an oxymoron.

But yet central bankers and other connected oligarchs think the big problem in our economy is that everyday people are getting 5% wage increases in a time of 4% inflation? As Jon Stewart told former Treasury Secretary Larry Summers recently - you guys need to get real about what's happening here.Hey @SeanDuffyWI - I’ve been seeing you

— JakeEdwards (@JakeMadtown) March 15, 2023

give Trump that dreamy-eyed stare a lot this week.

I’m sure you and your wife are mentioning your support of bank deregulation all over Fox this week. #wiunion #WI07 #wipolitics pic.twitter.com/7g3eDUHXCd

Danger! Workers are doing too well! Call the Fed to shut that down! A conversation with former Treasury Secretary Larry Summers. Watch the full interview in our latest episode, now streaming on @appletvplus. pic.twitter.com/B6GtO0QLnw

— The Problem With Jon Stewart (@TheProblem) March 17, 2023

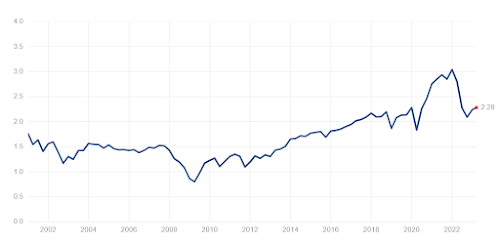

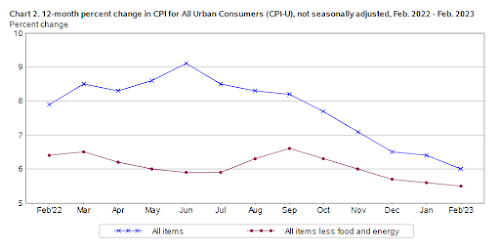

The Consumer Price Index (CPI) revealed headline inflation rose 0.4% over last month and 6% over the prior year in February, a slowdown from January's 0.5% month-over-month increase and 6.4% annual gain. Both measures were in-line with economist expectations, according to data from Bloomberg. The 6% jump in inflation marks the slowest annual increase in consumer prices since September 2021. "Core" inflation, which strips out the more volatile costs of food and energy, rose 0.5% over the prior month in February and 5.5% over last year, marking the smallest 12-month increase since December 2021. Economists had estimated "core" inflation would rise 0.4% on a month-over-month basis and increase 5.5% compared to February 2022.You can see the steady decline in the 12-month price change since inflation peaked in June.

For most goods and services, the process of recording prices is relatively simple: The bureau sends someone to a store, or calls a business, to see what they are charging for a bag of rice or to send a plumber out to repair a leaky faucet. Recording housing prices isn't as straightforward. The bureau measures actual rental rates for houses, and, using that data, estimates how much owner-occupied houses would rent for if they were put on the market. “It's a little bit of a fuzzy metric,” said Ryan Sweet, chief U.S. economist at Oxford Economics. OER is effectively the rent that the homeowner is giving up by living in their house instead of renting it out. It’s influenced by housing prices, but not directly tied to it…. As a result of its methodology, the all-important OER measure tends to lag behind movements in nationwide home prices by about a year. It took a long time for the pandemic-era surge in home prices to show up in the Consumer Price Index, and it will likely take a long time for the recent cooling of the housing market to show up as well.So this will also mean that CPI will cool down in the coming months based on this lagging OER measure alone. And given that many Americans are locked into fixed-rate mortgages and/or year-long leases, it is unlikely that they actually paid 0.8% more in shelter costs in February 2023. Then on Tuesday, we got information on Producer Prices, and that had even better news for those worried about inflationary pressures.

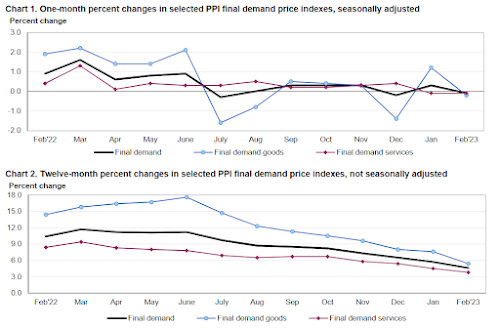

A key measure of inflation fell dramatically in February, according to the latest Producer Price Index, which tracks what America’s producers get paid for their goods and services. Producer price increases slowed to an annual pace of 4.6% last month, significantly lower than the downwardly revised 5.7% in January, the Labor Department reported Wednesday. February prices fell by 0.1% after rising by a downwardly revised 0.3% in January. Economists surveyed by Refinitiv had been expecting the 12-month rise in wholesale prices to slow to a 5.4% increase. Taking out the often volatile food and energy components, core PPI also notched some stark declines: Annual price increases dropped to 4.4%, and the index was unchanged from the month before (0% growth). Those are down from January’s downwardly revised 5% annual price gain and 0.1% monthly increase.So businesses aren’t seeing their costs for products in going up. That declining trend in PPI has been going on since June, with no one month having an increase in final demand above 0.3%.

Aaron Rodgers says on @PatMcAfeeShow: "Since Friday, my intention was to play and play for the NY Jets."

— Ian Rapoport (@RapSheet) March 15, 2023

No surprise on any of this, and of course Rodgers did it in typically eye-rolling fashion - using his segment on the Pat McAfee Show to make the announcement, with a nice side-order of victimization.Rodgers also says the deal is not done. But it's a matter of getting it done by this point, as the #Jets and #Packers work it out. https://t.co/bj1zAJDX5n

— Ian Rapoport (@RapSheet) March 15, 2023

underrated part of that interview... Aaron Rodgers said he was 90% retired heading into the darkness retreat and implied that the fact that the #Packers wanted nothing to do with him after, inspired him to want to play again and win (elsewhere with #Jets).

— Mike Obermuller (@obermuller_nyj) March 15, 2023

So Rodgers went from 90% retired (pre-darkness) to wanting to play for the #Jets. Interesting turnound. Sounds like a guy who is motivated to prove the #Packers wrong. @PatMcAfeeShow

— Rich Cimini (@RichCimini) March 15, 2023 Rodgers was leaning toward retirement when he arrived at the darkness retreat? I don't buy that for a second, and then he claims he only found out the Packers were looking to trade him when he came out of there a couple of weeks ago? Riiiiight. As a Packer fan, this was a long time coming, starting with the original sin of drafting Jordan Love in the first round back in 2020 - a stupid move that pissed off Rodgers and wasted a chance to immediately improve a team that was one game away from the Super Bowl. Rodgers responded with 2 great seasons in 2020 and 2021, but he also flamed out in the playoffs in both years (he was outright bad in that Niners game in 2021). Then things got worse. One year ago today, it seemed like the Packers were going to go full out for one last chance at a title when they signed Rodgers to a 3-year, $150 million contract extension. Which made it all the more perplexing when the Pack traded All-Pro receiver Davante Adams for draft picks a few days later. After the mixed messages that the team gave going into the 2022 season, there was definite decline for both Rodgers and the team, with the year ending with another loss at Lambeau in a win-or-go-home game.This just seemed like a relationship that had run its course. It happens, both in sports and in life. I just hope the Pack get a 1st round draft pick in THIS year's draft and other usable assets in return for trading Rodgers to the Jets, and that's what I'm paying attention to in the coming days and weeks. Likely in the next few years, the memories of Rodgers diva behavior and tech-bro-type weirdness and conspiracy theories should fade for me, and I'll remember Aaron Rodgers for on-field brilliance that I would argue even surpassed Brett Favre's career (Rodgers never had the level of INTs and meltdown games that Favre had). I hope I'll be fired up to see him enshrined in Canton some time in the early 2030s. But for now, I'm just glad this saga is winding down.Reminder that Aaron Rodgers’ last pass as a Packer (for now) is was an interception caught by @JKERB25 pic.twitter.com/aJ8iyDjrEW

— Barstool Illini (@BarstoolILL) March 15, 2023

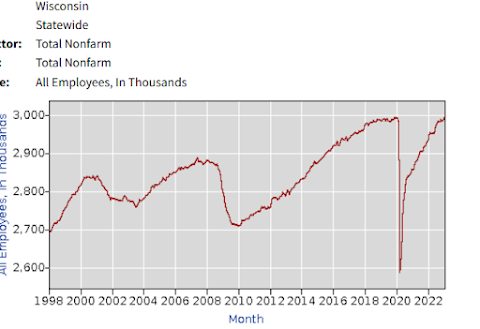

The Department of Workforce Development (DWD)...released the U.S. Bureau of Labor Statistics (BLS) preliminary employment estimates for the month of January 2023, which showed Wisconsin added 4,100 nonfarm jobs over the month and 55,800 jobs over the year. The data also showed that Wisconsin's unemployment rate fell to 2.9% for January, down 0.1 percentage point from the revised 3% in December 2022. The state's labor force participation rate for January was 64.5%. Nationwide for the month of January, the unemployment rate was 3.4% with a labor force participation rate of 62.4%.Pretty good situation to be in, to be sure. The reason we didn't find out about January's state jobs numbers until last week is because of the annual benchmarking for state figures, which follows data from the "gold standard" Quarterly Census of Employment and Wages (QCEW). Those figures run through the end of September, and came out on a statewide level in late February. With a year's worth of revisions, we can get a more accurate look at where our jobs market has been, and is at today. What we find is that Wisconsin did not have the losses that were initially reported for the end of 2021, and instead jobs went up by nearly 29,000 between July 2021 and January 2022. After while January gains were revised down slightly (by 5,000), we still added nearly 57,000 jobs last year. And we are well ahead of where we thought we were with the original data.

• Individual income tax refunds more than doubled, rising by $68 billion, thereby reducing net receipts. The precise timing of refund payments varies from year to year, but most will be paid in the period from February through April. The Internal Revenue Service reports that the number of refunds issued through the fourth week of February was 18 percent greater than in the same period in 2022. Average amounts refunded so far in 2023 are about 11 percent smaller, in part because the pandemic-related recovery rebates (also known as economic impact payments) and the expanded child tax credit have expired. … • Remittances from the Federal Reserve decreased from $48 billion to less than $1 billion. Higher short-term interest rates raised the central bank’s interest expenses above its income, eliminating the profits of most Federal Reserve banks.That's some of the reason for the jump in the deficit. But increased spending also is playing a significant role, led by the “big 4” – Social Security, Medicare, Medicaid, and Interest on the debt, and a one-off item.

The largest increase in outlays was related to receipts from the auction of licenses to use the electromagnetic spectrum. Proceeds from such auctions are recorded in the budget as offsetting receipts—that is, as reductions in outlays. In the first five months of fiscal year 2022, receipts totaled $81 billion—all recorded in January. No such receipts were collected during the first five months of 2023, resulting in a net increase in outlays.What's concerning is that this big jump in overall spending is happening as other areas of “spending” are being cut due to the end of COVID-era stimulus.

Outlays for certain refundable tax credits totaled $84 billion—a decrease of $69 billion, or 45 percent. That reduction occurred because the expanded child tax credit has expired. (In tax year 2021, eligibility for and the size of the child tax credit were expanded, and advance payments were made between July and December 2021.) Outlays from the Public Health and Social Services Emergency Fund decreased by $34 billion (or 66 percent), as expenditures decelerated for several pandemic-related activities, including reimbursements to hospitals and other health care providers, spending on coronavirus testing and contact tracing, and development and purchase of vaccines and therapies. Spending by the Small Business Administration decreased by $15 billion, or 94 percent. In the first five months of fiscal year 2022, that agency recorded nearly $16 billion in outlays, mostly for disaster loans and for grants to operators of shuttered entertainment venues. Those outlays declined toward the end of fiscal year 2022, and there has been little such spending in the current fiscal year.As mentioned earlier, there is some more fiscal restraint coming in Spring 2023, with expenses in SNAP and Medicaid likely to level off and decline vs last year as those expanded benefits and automatic enrollments in those respective programs go away in March and April. While that's good fiscal news, the deficit is still certainly on the rise, and the higher interest rates complicate this due to adding expense onto the debt. Which makes for a chicken-egg question about whether the higher deficits lead to higher inflation, and so that’s why the Fed should keep rates high to slow down that type of inflation (I generally disagree witht his idea, other than deficits leading to some higher demand). Or does it mean the Fed should back off on these higher interest rates because it’s causing higher expenses and making the deficit “problem” worse? (that's where I'm at) The higher refunds is also something to look at, both now and in the future, because extra added refunds might mean more “extraordinary measures” have to happen by the Treasury to keep from going over the debt limit, since more cash is going out the door. Or we hit the debt limit sooner, and/or refunds get slowed down to stay at/under that limit. It also definitely means this isn't the time to bail out one Silicon Valley Bank and the boom-bust tech and start-up schemes that those funds were pulled into. Not only is it rewarding sketchy business procedures, we also literally might not have much money available to do it, at least in the coming months.

JUST IN: Another hot jobs report! -- The US economy added 311,000 jobs in February, beating expectations. January’s blockbuster number barely revised to 504,000.

— Heather Long (@byHeatherLong) March 10, 2023

Unemployment rate up slightly to 3.6%

Wages rose 4.6% in the past year (cooling off some, but not much)

So this might be the first indication of all of the reported tech layoffs appearing in the jobs reports. Also note that services continue to see jobs come back (especially in hospitality sectors), and even retail recovered after losing jobs through much of 2022. February is also a good month to look at for another reason, because February 2020 is when employment peaked before the COVID-related shutdowns and adjustments. We exceeded that February 2020 peak last June, and are now up by nearly 3 million jobs (and 3.355 million in the private sector).Strong hiring across the board in February, except for warehouse & IT:

— Heather Long (@byHeatherLong) March 10, 2023

Hospitality +105,000

Retail +50,000

Gov't +46,000 (K12 educ. +23k)

Biz +45,000

Healthcare +44,000

Construction +24,000

Social assistance +19,000

**Transport/warehouse -22,500**

**IT was down -25,000 jobs**

The best news in the job report? More people are looking for work.

— Heather Long (@byHeatherLong) March 10, 2023

419,000 people entered the labor force in February.

The unemployment rate went up b/c more people are looking for jobs, not b/c of layoffs.

This is good news. More workers are returning. pic.twitter.com/yphqeu1WCA

But the overall employment-population ratio is down by nearly a full point compared to February 2020, which is indicative of the demographic challenges and post-COVID changes that have happened in this country. So we really don't have a large number of prime-age workers on the sidelines, but we do have more people to serve with less people available to do so. That could be a good thing for workers, because it may make it more difficult to lay people off and/or have them suffer through longer lengths of unemployment, because the demands remain with fewer workers available to replace and/or compete for open positions. But hourly wage growth also moderated (+0.24%), and really isn't causing any type of wage-price spiral. Combine it with the best job growth in decades, and it's something that both central bankers and workers should be happy about.For months, we've been asking where are the workers?

— Heather Long (@byHeatherLong) March 10, 2023

Well...the prime-age workforce (ages 25 to 54) is now back to its pre-pandemic level.

This is encouraging. It means we might be able to cool off the job market without needing to lay a ton of people off. https://t.co/rsjwChgY21

As I've said before, why would we keep jacking up rates to stop what seems to be a great economic situation? In February 2023, it looks like we continued to have strong job growth, good wage growth, and nothing to stop inflation from continuing to drift down from its highs in June. Let's take it and keep on rolling.It still remains stunning to me that we're experiencing one of the fastest paces of sustained job growth in our history during a period in which doom-and-gloomers and recessionistas dominated our headlines.https://t.co/0h4D3TsEcH

— Justin Wolfers (@JustinWolfers) March 10, 2023

The proposal also calls for the biggest spending increase on record when all types of state revenues are considered. The state’s so-called “all funds budget” includes GPR revenues, federal aid, segregated revenues such as the gas tax and hunting and fishing licenses that flow into stand-alone state funds for transportation and conservation, and program revenues such as university tuition and inspection fees. As shown in Figure 3, the proposed expenditures across all state funds would rise by a historic 17.9% over base levels in 2024 to $52.1 billion, before a slight decline of 0.8% to $51.7 billion in 2025….The Policy Forum says both Evers’ budget and the GOP’s flat tax scheme are both unsustainable, as they will have spending exceed revenues in 2025 and future years. And that the flat tax scheme is more damaging to the budget long-term.In the first year of the budget, while both GPR (up 23.2%) and federal revenues (21.9%) would account for by far the largest portions of the all funds spending increase, there would also be increases in program (6.2%) and segregated (2.7%) revenues. However, all types of revenue except federal would peak in FY 2024 and slightly decline in FY 2025.

Under the governor’s proposal, however, the state would draw down its general fund balance to help cover new spending on education, local governments, transportation, and a variety of other priorities. As Figure 5 shows, the drawdown would occur because proposed spending exceeds revenues by nearly $5.2 billion in 2024 and $1.3 billion in 2025. That would amount to the largest imbalance of any budget on record…. Republicans have said that they will remove or reduce many of the governor’s spending increases, which on its own would lessen the drawdown of state reserves and make the budget more sustainable. However, Senate Republicans favor a plan to shift the state’s income tax to one flat rate, a proposal which as we previously noted would lower state revenues by a projected nearly $5 billion over the 2023-25 budget and then by $9.4 billion in the 2025-27 budget, even before any cost to continue current services had been considered. This would likely make the overall budget even more difficult to sustain.Which probably explains why the WisGOP Chairs of the Joint Finance Committee are already saying they're not likely to put the flat tax in the budget, because they know what a fiscal and political loser it is. The Policy Forum also puts numbers and pictures behind the skyrocketing amount of surplus funds that are in the state’s bank and savings accounts.

Over the past two decades, Wisconsin’s budget reserve totals have gone from being one of the very worst in the country to being well above average. The state’s general fund is projected to close the 2023 fiscal year on June 30 with a balance of nearly $7.1 billion and a rainy day fund balance of $1.7 billion. The total reserves of more than $8.8 billion would be more than 1,900 times larger than at the close of 2005 and amounted to an unprecedented 44.7% of 2023 general fund spending, or gross appropriations. That is the highest level in Forum records going back 40 years.