1 day before the Federal Reserve will likely put in another rate hike in an attempt to tame inflation, we found out that

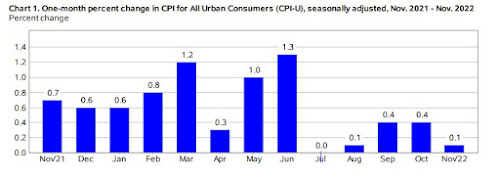

inflation in November...was pretty tame. The consumer price index, which measures a wide basket of goods and services, rose just 0.1% from the previous month, and increased 7.1% from a year ago, the Labor Department reported Tuesday. Economists surveyed by Dow Jones had been expecting a 0.3% monthly increase and a 7.3% 12-month rate.

The increase from a year ago, while well above the Federal Reserve’s 2% target for a healthy inflation level, was tied for the lowest since November 2021.

Excluding volatile food and energy prices, so-called core CPI rose 0.2% on the month and 6% on an annual basis, compared with respective estimates of 0.3% and 6.1%.

The core increase of 0.2% is something that the Fed gives extra creedence to, and is the lowest one-month increase since August 2021. The all-product inflation number was even lower than the core figure, as gas prices retreated after the election, and that number has been tame for the last 5 momnths.

With this latest evidence that

INFLATION PANIC is fading out,

the stock market reacted as you would have thought at the opening (although it didn't end that way).

The benchmark S&P 500 (.SPX) jumped as much as 2.76% to a three-month high early in the trading session on news that November U.S. consumer prices barely rose as gasoline and used cars cost less, leading to the smallest annual inflation increase in nearly a year at 7.1%.

Rising expectations for smaller and slower Fed rate hikes sent U.S. Treasury yields sharply lower and helped lift rate-sensitive gauges like the S&P 500 growth index (.IGX), up 1.18%, and the S&P 500 real estate index (.SPLRCR) up 2.04% to their highest intraday levels in nearly three months. The real estate sector notched its biggest daily percentage gain in two weeks as the best performing of the 11 major sectors....

Still, equities pared gains ahead of the Fed's policy statement on Wednesday, in which the central bank is widely expected to announce a 50 basis point rate hike.

"There was some excitement early on that the CPI number was once again below expectations - it shows some sequential cooling - but once we saw that initial pop, stock investors kind of reassessed," said Jason Ware, chief investment officer at Albion Financial Group in Salt Lake City, Utah.

The lower gains were due to worries that Fed Chair Jerome Powell is going to keep on raising rates well beyond the 50 points that are expected for tomorrow. But if we're seeing consumer prices rise by a total of 1% over 5 months (aka an annual rate around 2.5%), why would keep raising rates past the 4.25% they're going to be at after tomorrow?

That doesn't mean inflation concerns are over, and the 0.5% increase in food at home for November (and a 12% rise in that sector over the last 12 months) shows that many Americans are still dealing with annoyances and hardships in some areas. But with gas prices falling further in December, and

producer prices continuing to level off (and go down further up the supply chain), it sure seems like we're in a much more stable place compared to June, doesn't it?

Let's hope that the Fed has looked at these real-world numbers, and stop pretending that we are in the same situation we were in at the start of the Summer. We are in a balanced economy that still is gaining jobs with inflation being back toward normal, but are near capacity and are seeing housing and construction start to falter. At this point, there isn't much inflation to put a lid on, so why would we keep tightening up to fight a "problem" that already seems to be under control?

No comments:

Post a Comment