JUST IN: The US economy added 263,000 jobs in November – another month that blows bast expectations of 200,000. The job market is still pretty hot.

— Heather Long (@byHeatherLong) December 2, 2022

Unemployment rate stayed at 3.7% (up slightly from 3.5% in in Sept.)

Wage growth: 5.1% for past year --> better than expected

But that 5.1% wage growth and 0.6% increase in average hourly wages for November gave some Wall Streeters cause for concern because it keeps them on INFLATION WATCH!In November, the economy added jobs about everywhere except retail/warehouse

— Heather Long (@byHeatherLong) December 2, 2022

Restaurants +62,000

Healthcare +45,000

Gov't +42,000

Social assist +23,000

Construction +20,000

IT +19,000

Manufacturing +14,000

'Laundry services' +11,000

Biz +6,000

Warehouse -13,000

Retail -30,000

Labor market tightness and strength keeps the Fed on its monetary policy tightening path at least through the first half of 2023, and could raise its policy rate to a higher level where it could stay for sometime. It also underscores the economy's resilience heading into was is expected to be a tough year. "November's labor market report was clearly bad news for the Fed's war on inflation," said Jan Groen, chief U.S. macro strategist at TD Securities in New York. "The Fed has no other choice than to remain in tightening mode for the near future, with 50 basis points hikes in December and February." Nonfarm payrolls increased by 263,000 jobs last month. Data for October was revised higher to show payrolls rising 284,000 instead of 261,000 as previously reported. Monthly job growth of 100,000 is needed to keep pace with growth in the labor force.Not mentioned is that September was revised down by 46,000 to 269,000, so we're in a lower (but still strong) rate of job growth. I'll also note that the average work week went down by 0.1 hours, so weekly wages were only up 0.26% last month - good enough to keep up with prices, but not enough to boost inflation back up (well, at least in a non-profiteering way). Likewise, we got another report this week showing inflation had stayed in line through October.

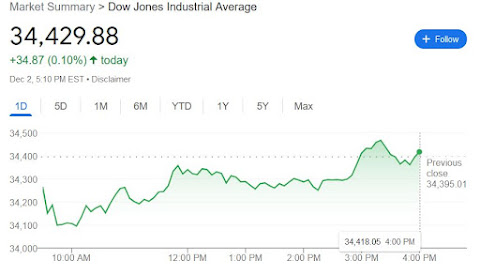

A gauge of inflation that top economic policymakers monitor showed price gains slowed in October, the Commerce Department said on Thursday.... By the numbers: The Personal Consumption Expenditures (PCE) index, the Federal Reserve's preferred gauge of inflation, rose 0.3% in October — as it did in August and September. Prices rose 6% over the year through October, slowing from the 6.3% registered in September. It's the so-called "core" measure of inflation, which strips out volatile food and energy costs, that cooled notably. Core PCE rose 0.2% in October, after two consecutive months of 0.5% increases. Prices rose 5% from October 2021, compared to the 5.2% in September.That PCE index is up a total of 0.8% in the last 4 months measured, and the "core" measure is 1.3% in that time. That's around a 2.5% annual inflation rate and 4% core rate, and that was a month before we saw gas prices fall below $3 a gallon in these parts. In a logical world, why would you want interest rates to go much above the 3.75%-4% Fed Funds rate that we are at today? I know there will likely be a rate hike in December, but does the data tell us that there is any reason to keep jacking beyond that, and cause a full-blown hard recession vs the "soft landing" that it seems like we are heading toward today? I say no. And I think Wall Street traders figured that out as the day went on, with the DOW pulling out a gain after falling 300 points immediately after the Friday morning release of the jobs report.

No comments:

Post a Comment