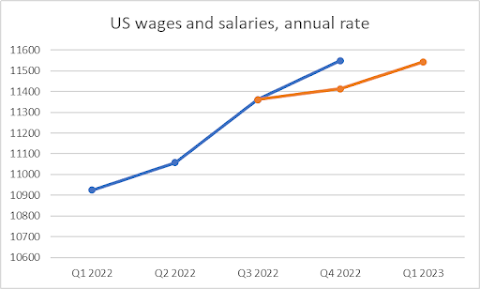

Real gross domestic product (GDP) increased at an annual rate of 1.3 percent in the first quarter of 2023 (table 1), according to the "second" estimate released by the Bureau of Economic Analysis. In the fourth quarter, real GDP increased 2.6 percent. The GDP estimate released [Thursday] is based on more complete source data than were available for the "advance" estimate issued last month. In the advance estimate, the increase in real GDP was 1.1 percent (refer to "Updates to GDP"). The updated estimates primarily reflected an upward revision to private inventory investment. The increase in real GDP reflected increases in consumer spending, exports, federal government spending, state and local government spending, and nonresidential fixed investment that were partly offset by decreases in private inventory investment and residential fixed investment. Imports, which are a subtraction in the calculation of GDP, increased.As mentioned in my observation about the income and spending report, the growth in wages and salaries was revised down for the last 3 months of 2022. In fact, total wage and salary income in Q1 2023 is no different than what was originally reported for Q4 of last year.

Profits from current production (corporate profits with inventory valuation and capital consumption adjustments) decreased $151.1 billion in the first quarter, compared with a decrease of $60.5 billion in the fourth quarter (table 10).

Conflicting Signals for Coincident Macro Indicators (incl @NBERPubs BCDC) at End-May: labor market, cons'n, personal inc up in April; but GDO and GDP+ down in last two qtrs @SPGMIFinancials @PhiladelphiaFed @AtlantaFed https://t.co/ZYT8ZHxx3H pic.twitter.com/uDsaGLXmLY

— Menzie Chinn (@menzie_chinn) May 26, 2023

Given the NBER Business Cycle Dating Committee’s emphasis on employment and personal income, one would be fairly confident that no recession was in place as of April 2023, of course keeping in mind all these numbers will be revised over time. GDP in particular will be revised numerous times so an increase in this series would not be decisive in ruling out a recession (just as the decline in 2022Q1-Q2 would not be decisive in ruling in a recession). We know that reported GDP is actually not the best indicator of where GDP will eventually be revised to. GDO and GDP+ are two series are more likely to fulfill that condition. Here, we see some troubling signs. While GDP was revised up to 1.3% SAAR, GDO (the average of GDP and GDI) and GDP+ are at -0.5% and -1.2% SAAR, respectively. As Jason Furman has noted, the discrepancy between GDP and GDI is very large, highlighting the uncertainty we face discerning how economic activity trending. This shows up in a discrepancy in the bean counting exercises, with GDPNow at 1.9% SAAR, but SPGMI (formerly Macroeconomic Advisers and IHS Markit) at 0.4% — essentially zero.If we don't have any monkey business that keeps the debt ceiling from being raised, these are the underlying factors that we can continue to look at to see where the US economy heads for the rest of 2023. Decent spot for now, but we'll see if the consumer can hold up the strong results we've been seeing so far this year.

No comments:

Post a Comment