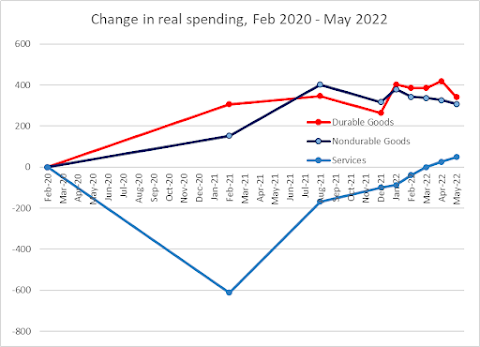

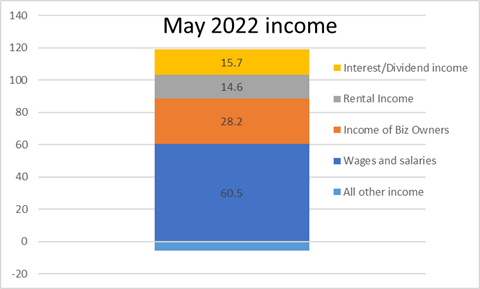

Personal income increased $113.4 billion (0.5 percent) in May, according to the Bureau of Economic Analysis (tables 3 and 5). Disposable personal income (DPI) increased $96.5 billion (0.5 percent) and personal consumption expenditures (PCE) increased $32.7 billion (0.2 percent). Real DPI decreased 0.1 percent in May and Real PCE decreased 0.4 percent; goods decreased 1.6 percent and services increased 0.3 percent (tables 5 and 7). The PCE price index increased 0.6 percent. Excluding food and energy, the PCE price index increased 0.3 percent.Real consumption’s decline of 0.4% is bad enough, but this report also included downward revisions of March and April that totaled $104.4 billion (annual rate), so our previously-strong spending levels don’t seem so strong any more. Some economic journalists have noted that price growth seemed to be cooling some (only 0.3% core for May, and 4.8% core over the last 12 months), but even that comes with a caveat, because food prices were up 1.2% for May and energy goods and services were up 4.0% for the month, and overall 12-month PCE price growth went up to 6.7% from 6.5%. So still high, and it translates into real disposable incomes being down 3.3% over that year-long period. The only other positive in this report is that despite the lame overall consumption numbers, spending in services continues to come back. In fact, the last 4 months have seen a clear movement of spending habits into services and out of goods – which seems to indicate a reversion back toward pre-COVID World patterns.

It does seem that June has been a time of adjustment, not just in expectations from a jittery Wall Street, but also in an oil market that saw futures drop by $15/barrell over the past 3 weeks. We’ll find out next week if the adjustment includes a lesser-than-normal amount of Summer hiring, and if wages offered are also one of those adjustments. What’s clear is that we’re in a type of higher-inflation, near-capacity economy that I certainly haven’t dealt with in my adult life, and my fear is still that the Federal Reserve will care too much about the inflation side of the economy and overshoot. Which could well lead to serious damage in a “jobs-and-spending” side of the economy that may already be moderating on its own.The recent GDPNow forecast implies 1.07 pp contribution of final sales to domestic purchasers. It was 2.01 pp in Q1. The economy is slowing. But even with 2 negative quarters of real GDP growth in a row it doesn’t mean it is in a recession. The recession isn’t inevitable. pic.twitter.com/2sFUz4gEgI

— Paweł Skrzypczyński (@p_skrzypczynski) June 30, 2022

No comments:

Post a Comment