Manufacturing in the US has had a big comeback in the last 2 years, both in employment and activity. But

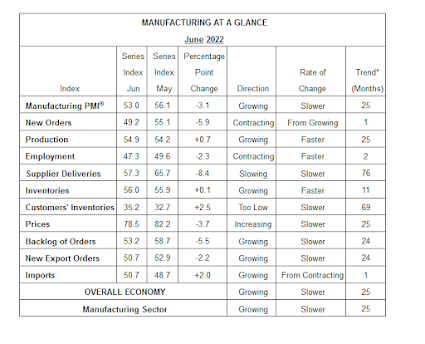

a new report on Friday showed that manufacturing’s previously-robust growth wasn’t so strong in June. "The June Manufacturing PMI® registered 53 percent, down 3.1 percentage points from the reading of 56.1 percent in May. This figure indicates expansion in the overall economy for the 25th month in a row after a contraction in April and May 2020. This is the lowest Manufacturing PMI® reading since June 2020, when it registered 52.4 percent. The New Orders Index reading of 49.2 percent is 5.9 percentage points lower than the 55.1 percent recorded in May. The Production Index reading of 54.9 percent is a 0.7-percentage point increase compared to May's figure of 54.2 percent. The Prices Index registered 78.5 percent, down 3.7 percentage points compared to the May figure of 82.2 percent. The Backlog of Orders Index registered 53.2 percent, 5.5 percentage points below the May reading of 58.7 percent. The Employment Index contracted for a second straight month at 47.3 percent, 2.3 percentage points lower than the 49.6 percent recorded in May. The Supplier Deliveries Index reading of 57.3 percent is 8.4 percentage points lower than the May figure of 65.7 percent. The Inventories Index registered 56 percent, 0.1 percentage point higher than the May reading of 55.9 percent. The New Export Orders Index reading of 50.7 percent is down 2.2 percentage points compared to May's figure of 52.9 percent. The Imports Index climbed into expansion territory, up 2 percentage points to 50.7 percent from 48.7 percent in May."

Fiore continues, "The U.S. manufacturing sector continues to be powered — though less so in June — by demand while held back by supply chain constraints. Despite the Employment Index contracting in May and June, companies improved their progress on addressing moderate-term labor shortages at all tiers of the supply chain, according to Business Survey Committee respondents' comments. Panelists reported lower rates of quits compared to May. Prices expansion slightly eased for a third straight month in June, but instability in global energy markets continues. Sentiment remained optimistic regarding demand, with three positive growth comments for every cautious comment. Panelists continue to note supply chain and pricing issues as their biggest concerns. Demand dropped, with the (1) New Orders Index contracting, (2) Customers' Inventories Index remaining at a very low level, though it increased and (3) Backlog of Orders Index decreasing but still in growth territory. Consumption (measured by the Production and Employment indexes) was mixed during the period, with a combined minus-1.6-percentage point change to the Manufacturing PMI® calculation. The Employment Index contracted for the second month in a row after expanding for eight straight months (September through April), but panelists again indicated month-over-month improvement in ability to hire in June. Challenges with turnover (quits and retirements) and resulting backfilling continue to plague efforts to adequately staff organizations, but to a lesser degree compared to the previous month. Inputs — expressed as supplier deliveries, inventories and imports — continued to constrain production expansion but to a lesser extent compared to May. The Supplier Deliveries Index indicated deliveries slowed at a slower rate in June, which was supported by a slight increase in the Inventories Index. The Imports Index expanded in June after one month of contraction preceded by six consecutive months of expansion. The Prices Index increased for the 25th consecutive month, at a slower rate compared to May.

Dig further into the report and you can see that the businesses said that new orders starting shrinking in June, and reported fewer jobs for the second straight month.

Not a great sign, although a slowing of backlogs and customers’ inventories not being as tight is a nice side effect. As I’ve mentioned before, some of these sectors could use a breather from the torrid demand of 2021 and early 2022 to buy time to get back toward a balanced, less-inflationary business situation.

But another blue-collar area segment also had a negative report on Friday, with

(seasonally-adjusted) construction activity having a surprising decline. U.S. construction spending unexpectedly fell in May as single-family homebuilding stalled, more evidence that the Federal Reserve's aggressive monetary policy tightening was slowing the economy.

The Commerce Department said on Friday that construction spending slipped 0.1% in May after increasing 0.8% in April. Economists polled by Reuters had forecast construction spending would rise 0.4%. Construction spending increased 9.7% on a year-on-year basis in May.

Spending on private construction projects was unchanged in May after advancing 1.1% in April. Investment in residential construction rose 0.2%, though spending on both single-family and multi-family housing projects was flat.

The construction decline is a big warning, especially if it’s an offshoot of higher interest rates. But it also comes on the heels of that sizable increase in April, and a 3.2% total increase over the 3 months between January and April. So this could merely reflect some projects moving forward ahead of the usual seasonal schedule, and we see a return to increased activity in June.

However, it comes after other subpar economic data for the week, so we can’t just blow these reports off. It's possible that the warm weather and

strong travel numbers are masking what’s a rough situation in other parts of the economy. Or, maybe I'm not sensing a bad economy because Wisconsin has been chugging along while other areas are struggling, as we saw in another report released this week.

This places Wisconsin 5th among US states for Q1 GDP, with a much smaller decline than the 1.6% drop in (inflation-adjusted) GDP for the country as a whole. And combined with our strong revenue picture, maybe this is why all of the panicky talk I hear in the financial news doesn’t match up with what I’m seeing as I go out and about.

But what if these manufacturing and construction figures are reflections of an economy that isn't just slowing, but actually in recession? And conversely, what if slowing demand and a freeing of backlogs is softening inflation? Then maybe Jerome Powell and company at the Fed should back off after a couple of more rate hikes and make sure they don’t trigger a truly bad economy with sizable job loss, instead of an overheated one that is merely reverting toward a post-COVID version of normalcy.

We can handle a slowing of growth or even a minor “recession” that’s really a meeting of shortages. But a big decline that leads to sizable job loss is worse than the annoying rise in prices we’ve had to deal with in the first half of 2022.

No comments:

Post a Comment